More on KentOnline

More on KentOnline

Homeowners in Kent are being urged to act now to prevent their monthly mortgage costs rocketing ahead of more predicted increases in interest rates.

Those near the end of fixed-term deals or looking to buy are reporting how they're already facing forking out hundreds of pounds more to cover the additional costs.

It comes after the British economy was rocked by Chancellor Kwasi Kwarteng's mini-Budget last week, which saw a flurry of tax cuts, fuelled by increased borrowing, and sent the value of the pound plummeting.

And that, in turn, has prompted the Bank of England to warn of "significant" increases to interest rates - which could end up adding hundreds of pounds onto monthly mortgage repayments.

Today the Bank announced it will step in to calm markets by buying government bonds on a temporary basis to help "restore orderly market conditions".

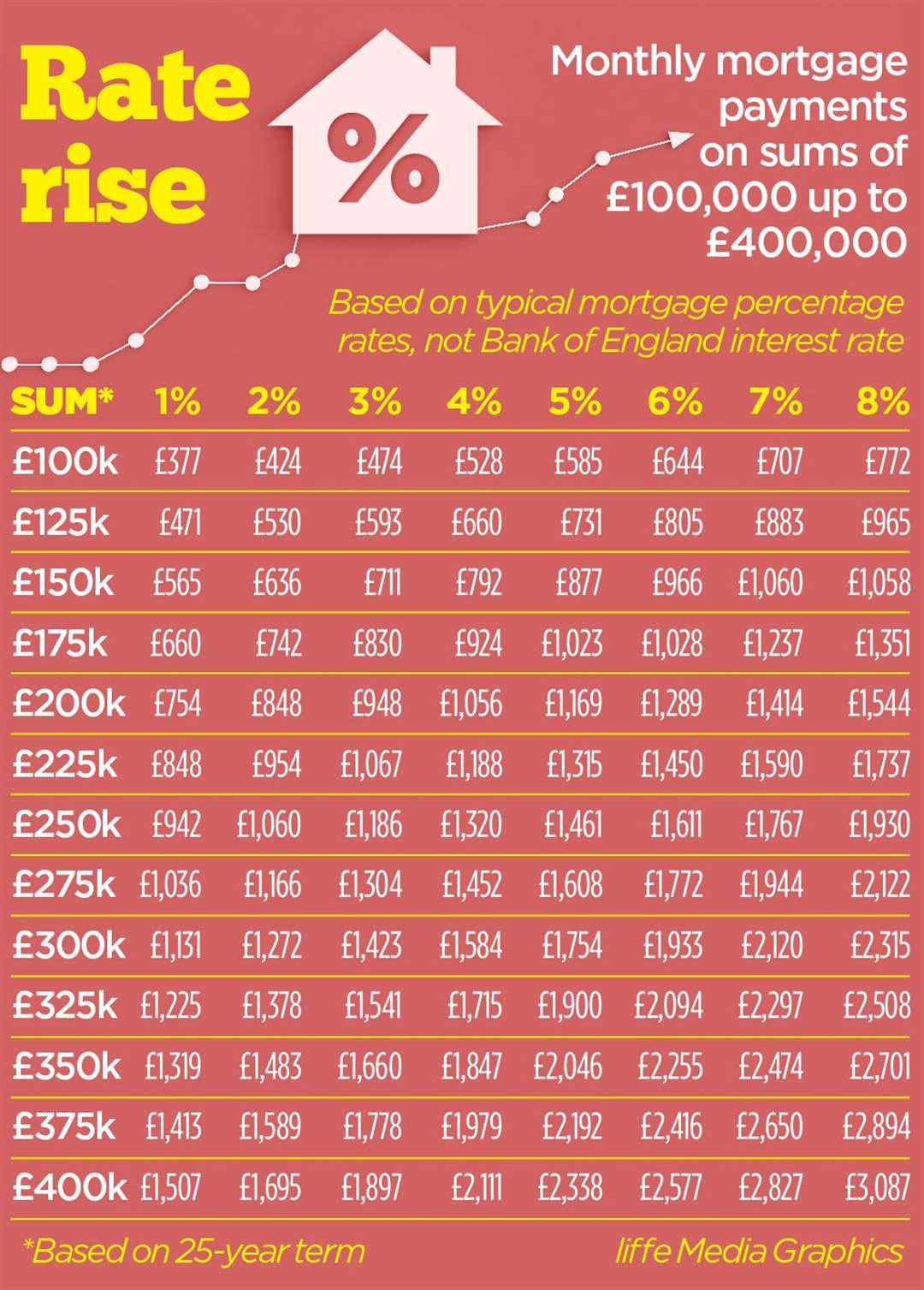

Some economists have predicted it will raise the interest rate from the current 2.25% to 5.8% by next spring.

Kerry Nash, director and mortgage advisor at Marble Financial Planning, with offices in Whitstable and Herne Bay, says there is currently an "element of panic".

She explained: "I've been in the industry for more than 20 years and the only time when it was a bit crazy like this was when Covid first started. However, then the rates were coming down quickly, so although there was a rush, the overall outcome was for the benefit of people.

"Now, they are going up and these increases are costing people between £50-100 each time it's happening.

"There's definitely an element of panic among people at the moment."

Kerry says earlier this week mortgage offers were being withdrawn by nervous banks "seconds after I was offering them to customers" .

"The mortgage will be their biggest debt," she said. "While the interest rate is going up a quarter of a percent, it may not sound too bad, but when you put that against a debt of an average between £200-300,000 that makes a significant difference to someone's monthly payments.

"We would hope at some point, when inflation is under control and things have settled down, the interest rates would start to come down as well.

"However, with all of the uncertainty at the moment it's a gamble. And when you're talking about your biggest monthly cost, increasing by £300-500 a month if you leave it any longer, the gamble is far too high.

"It could get to the point where people cannot afford their mortgage and that's when you could start to see repossessions, and that could affect the housing market as well."

The current Bank of England base rate is 2.25% - and while it is widely expected this will rise again over the coming days, there is mounting speculation it could reach as high as 6%. In December of last year, it stood at an historic low of just 0.1%.

Banks set their mortgage rates above this. Kerry says while the best deals were around 3% on Monday, today they are already getting closer to 4%, with Nationwide putting up its rates 1% overnight.

Interest rates are traditionally lifted in a bid by the Bank of England to control inflation. That is currently at 9.9%. The target is just 2% - a figure seen as the economy growing steadily and in line with people's wages.

"It's a big increase and the majority coming out of their deals now probably had interest rates which started with a one..."

Inflation is measured by a 'shopping list' of average goods and services used in the UK - ranging from fuel to groceries and restaurant prices. The inflation rate - in other words how much more expensive things have got - is measured by comparing one month to the same the previous year.

The argument goes that if rates go up, we tighten our belts and reduce our spending; borrowing money rates increase and thus demand for goods is reduced and prices, should, start to dip.

The government's mini-Budget last week rather flew in the face of attempts to bring inflation rates down.

Although energy price caps will reduce its rate of rise a little, by cutting taxes it puts more money in people's pockets which, in turn, encourages spending - the very thing the Bank of England is trying to limit.

Coupled with increased national borrowing to fund the cuts and the energy price cap, the markets have reacted with growing unease as investors now view the British pound as a less stable and reliable investment. Thus the price against the dollar - the standard comparison rate - fell to an all-time low earlier this week. Why does it matter to you? Well, a weakened pound against other currencies will increase prices as the pound doesn't carry the value it once did. Which, in turn, could fuel inflation.

It is a bleak and uncertain time for the economy.

As for householders, each change in the interest rates will have a significant impact on monthly repayments for those not on fixed-term contracts - often referred to as trackers (in other words they track the base rate - going up when it rises and down when it drops). And for those coming to the end of their existing fixed deal within 12 months, the advice is to act now.

Mortgage advisor Kerry said: "Almost all of the lenders will give a six-month mortgage offer - so if you start to look now and get something secured, you would have that valid now until March.

"You wouldn't have to act until the end of six months, but the banks will honour that rate. It gives people the chance to have something banked in case of any further rises over the coming months.

"On Monday and Tuesday the banks said they were withdrawing all of their mortgages so they could think about what they want to do. But these rates are not going to be coming out lower.

"It's a big increase and the majority coming out of their deals now probably had interest rates which started with a one. On average, most people we're dealing with are looking at increases, per month, of between £250-300 at the moment. Just for a like-for-like remortgage.

"It may even be worth people's while to look at paying an early repayment penalty to get out of their mortgage and get a new deal now with the rates they are at the moment."

Estimates of the interest rate rising to 6% would add around an extra £500 on monthly repayments for an average £200,000 mortgage.

"Our monthly outgoings could go up almost £800. It's a real struggle..."

One homeowner from Herne Bay, who spoke to KentOnline but did not want to be named, has 14 months left on his fixed-term mortgage - at 1.79% - but is considering securing a new deal early to avoid potentially catastrophic rates next year.

It would see his monthly payments increase from £823 a month to £1,139, based on a fixed five-year deal at 3.99% over 25 years.

"More than £300 a month is hard to swallow, but I worry what the rates could rise to if we wait and they shoot up even more, as a lot of people are predicting," said the married dad-of-two.

"Our energy bill has gone up £200 a month, and we recently had to get a loan to buy a car after our old one died, so in the space of six months our monthly outgoings could go up almost £800. It's a real struggle.

"We were advised to secure the mortgage deal at 3.99% as it's valid for six months, so we'll just wait to see how the picture changes before we commit.

"But if the dire forecasts are to be believed, it sounds like 3.99% might be an absolute bargain when it comes to the time we have to make a decision."