More on KentOnline

More on KentOnline

As house prices continue to soar can you guess which district in Kent has seen the biggest property price growth over the last 26 years? The answer may surprise you.

But before we get to that, earlier this week the Office for National Statistics (ONS) published figures which revealed the average house value in England hit a record £312,000 in July.

In the south east, the rise, over the course of the year, represented an eye-watering leap of 15.8%. Much higher, it should be pointed out, than London, which saw a rather more modest 9.2% increase - the lowest of all the regions in England.

The dramatic rise is, in part, due to a slump in the market last July following the end of the Stamp Duty holiday period - ushered in by the government to help stimulate the market after the ravages of the pandemic.

In Kent, the average property price now tops £331,000.

Which means if you wanted to get a mortgage, using the current rough guide of a lender providing you with around four times your salary, then you'd need to earn in excess of £80,000.

Given the average salary in the county is closer to £30,000 you can see the challenge that presents to those desperate to get on the housing ladder,

But then house prices being out of reach of many will come as little surprise; a whole generation have had to come to terms with it.

The question is, will they ever drop?

Spencer Fortag is a property expert who runs Dockside Property Services in Medway.

"I was going to say if something seismic happens it might bring prices down," he says, "but we've had lots of seismic things happen and it's not really dented people's confidence in property.

"The fundamental reason will never change - we have a safe, democratic society, there's never a challenge as to who owns the land and culturally and educationally we are revered across the globe.

"Because it's not just us islanders that buy our own properties - there's massive external, foreign, investment which wants to buy in the UK."

That has been witnessed in Kent's residential market by the influx of buyers from Hong Kong snapping up properties as they seek to start a life here.

"Having said all that," adds Spencer, "it is feasible house prices can one day fall.

"If, for example, we had a change of government and a policy restricting foreign investment, we may see a drop. If interest rates sky-rocketed into double digits, but then, of course, where one market suffers, generally the other benefits and that's true of the sales and rental market.

"Over the last few years I've given up predicting because we never know what's around the corner."

Hiked up interest rates, of course, send mortgage costs rising too.

Not that out-of-reach house prices was always the way.

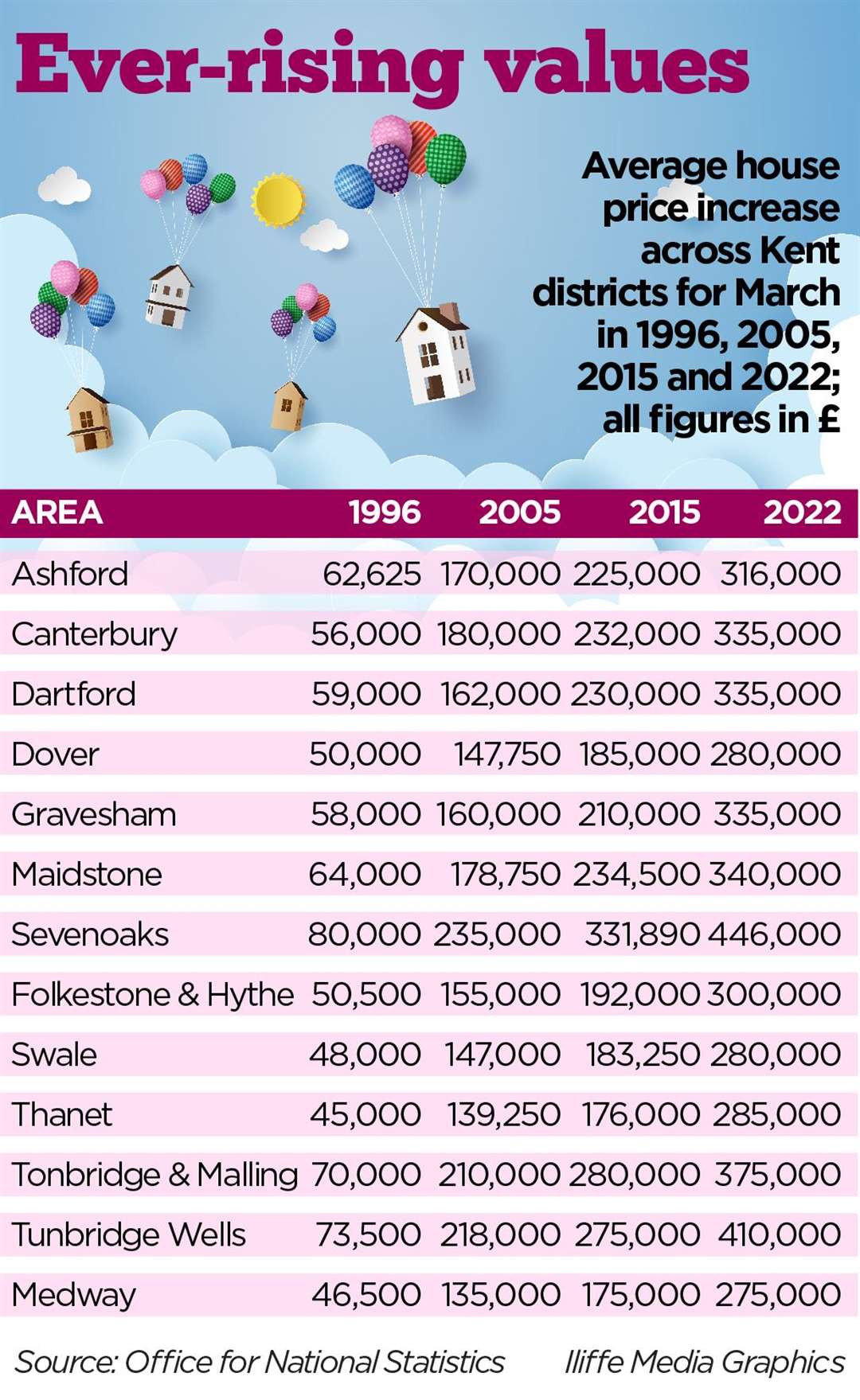

According to ONS figures, the median price of a residential property in, let's take the county town of Maidstone as an example, was £64,000 in March 1996.

At the time, you could almost certainly get a 100% mortgage. Chances are you could even borrow a little more so you could splash out on some furniture. Oh yes, younger readers, you could get lent all the money you needed (don't worry about the deposit) and some more to pay back at your leisure.

But the credit crunch of 2008 - caused after some rather reckless lending by the major US banks - saw a radical shake-up in the way money was handled to prevent a repeat of the financial crash it ushered in. The result was the near-death of the 100% mortgage and a requirement for deposits to absorb any potential future shortfall should property prices take a hit and leave lenders exposed.

Back to those Maidstone house prices. Within 10 years, that price, according to the ONS, had increased to £178,750. By March 2022 it stood at an eye-watering £340,000. That's an increase of more than 431% over the space of 26 years.

And it's far from the biggest percentage rise.

Want to know the district with the biggest leap? Well it's sunny Thanet. Property there in 1996 would have set you back an average of £46,500. Today it's £285,000.

Who says art - in the guise of the Turner Contemporary - can't be the catalyst for economic recovery?

In fact, seaside locations have proved a sound investment.

Canterbury was always popular, but the boom in Whitstable has played a significant role in the city district's average price rising from £56,000 in 1996 to £335,000 today. A rise of 498%.

Next is Folkestone and Hythe, where property prices are up six-fold from £50,500 to £300,000.

If you purchased a property in the east of the county, it seems, you're quids in.

Rob Sabin, sales director at estate agents Miles and Barr, said: "East Kent covers a wide area with a variety of towns and locations that appeal to a broad selection of buyers.

"The region's diverse lifestyle offering, variety of housing options and broad property price range, means it can outperform national trends. The east Kent housing market continues to remain buoyant because people still like the appeal of living by the coast with the benefit of great transport links back to London. This continues to be a major pull factor for many homebuyers."

Mind you, the east doesn't take all the top spots.

The lowest return on investment is in Ashford ,where prices started at £62,625 and have risen to £316,000 - still, it should be said, a healthy increase for owners of 405%.

Other big increases are in the likes of Medway, Swale and Gravesham.

And, it goes almost without saying, the highest prices are in the commuter heartlands in the west. The average Sevenoaks property earlier this year was £446,000; Tunbridge Wells £410,000 and neighbouring Tonbridge at £375,000.

All of which is great news if you're a home owner sitting on an ever-increasing priced property. Yet it's a body blow for those saving frantically in a bid to get on the housing ladder.

"There is an absolute shortage of properties to buy at the moment within Kent," says Spencer Fortag, as to why prices are so high.

"Despite the fact we are seeing some new-build developments come online, the fact remains there is a strong and continued massive demand for property.

"We're nowhere close to satisfying that appetite.

"All local councils have targets to meet - Kent and Medway is not alone in that respect - neither are they alone in not meeting those targets that have been set by central government.

"We're just not building enough new and affordable homes."

Which may sit uncomfortably with those who object to the scale of new housebuilding in the county.

As for the immediate future? He may not like trying to predict what lurks around the corner in an ever-more uncertain world, but Spencer believes despite the cost-of-living crisis and increasing interest rates - which hike up mortgage payments - things will stabilise.

He explains: "I think what we'll see is Medway and Kent house prices will remain broadly neutral over the next 12-18 months.

"The two main drivers behind house prices are employment levels and interest rates. Currently, employment levels seem pretty stable and interest rates are certainly manageable and on the low side, despite recent increases.

"If we don't see massive disruption to employment levels and interest rates shooting up, I remain fairly confident house prices will remain stable.

I remain fairly confident house prices will remain stable.

"But watch this space. The final quarter of this year will be a challenging time for lots of people."

And that may, just may, peg back the ever escalating cost of properties. Just don't bank on it.