More on KentOnline

More on KentOnline

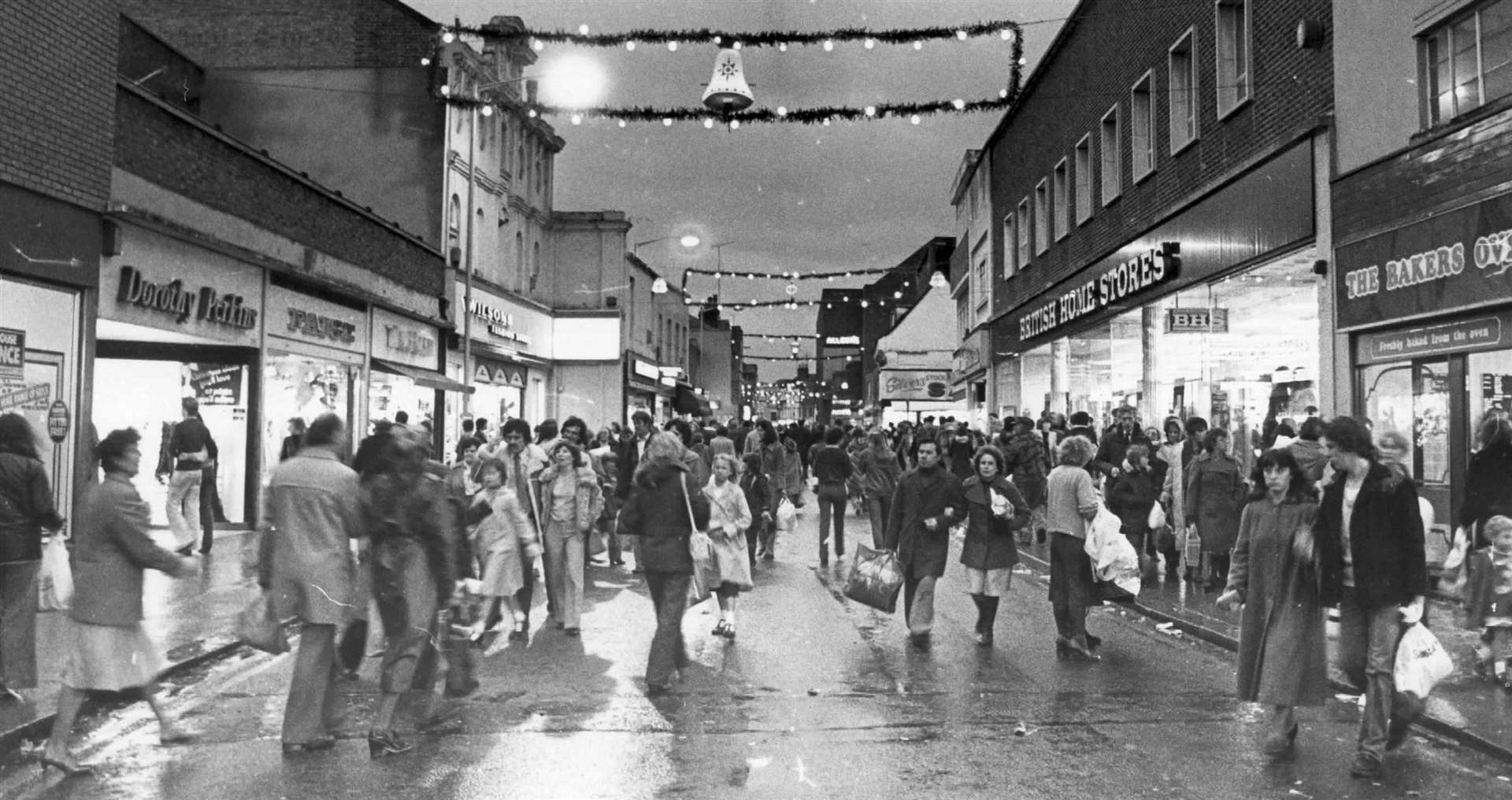

For many of us, our memories of the county's high streets and town centres are one of vibrancy.

Stores were busy, streets crowded, car parking a pain, but, above all, it was the place to go and, for the younger generation, the place to be seen.

But a lot can change and, over the past 30 years, that has perhaps never been most pronounced than in the retail hearts of our communities.

Today, many high streets are pockmarked by empty shop fronts – 'to let' signs hung more in hope than expectation. The hustle and bustle has gone, the shared experience no more.

Now they face an existential threat which would have seemed ludicrous to those growing up in the 1980s, when our lust for the in-person consumer experience was at its peak.

While many point the guilty finger simply at the surely irreversible rise and rise of online shopping, the reality is there are myriad other factors which all contributed to play a key part. And the rot set in earlier than you would perhaps imagine.

Traditionally, our town centres were the glue which held our communities together.

Whether you lived in a town's urban sprawl or outlying village, you would gravitate towards a central high street for the majority of your shopping needs. Supermarkets were there, cinemas, and all the other amenities we needed.

But then, during the late 1980s, the supermarkets started to covert more space – both internally and for their shoppers' motoring needs. In order to expand they turned their back on the expensive rents of town centres, and opted, instead, to create out-of-town superstores. There they could dramatically broaden their offering and, crucially, lure in shoppers with free car parking they could easily access with their laden trolleys.

From Ashford to Dover to Gravesend, the big supermarket chains migrated. Things would never be the same again.

From books to CDs to clothes, economies of scale meant supermarkets could, in a pre-internet era, easily trump the price of high street retailers and all in the most convenient of covered settings. They all wanted to be one-stop shops for everything we needed.

Many of the traditional town centre stores started to feel the ground beneath them shake.

Supermarkets, happy to slash prices on the biggest new release books and albums so they lost money (so-called 'loss-leaders') did so safe in the knowledge that while in their cavernous stores, sufficient profits would be accrued on other items picked up at the same time. The die was cast.

Keen to go where the customers were flocking, these big out-of-town supermarkets were joined by other major retailers.

Many bemoaned the impact on town centres, but with all capitalist progress, the proof was in our spending habits – and they were going out-of-town too.

For Kent's towns it is worth noting that the Nineties was book-ended by two major openings – Lakeside, a short hop-skip-and-a-jump over the Dartford Crossing in 1990, and in 1999 by Bluewater. Both were transformative for nearby towns – sucking out many big name retailers and providing a US mall-style experience, complete with restaurants and sprawling multiplex cinemas.

While high streets felt the pinch, with 50 years of growth behind them, they felt confident they could rebound.

In fact, to combat the scale of the new breed of superstores popping up, investors – and it's important to note here these were almost always big property companies and not local authorities – decided to boost their town-centre offerings.

As the Noughties dawned so did plans to upgrade existing town centres to adjust them for a more demanding consumer.

And they had to because as we demanded big covered shopping complexes with big stores and free parking, investors looked to re-create town centres in out-of town developments.

Where Hempstead Valley in Medway had pioneered the concept in the late 1970s (it was the first to open in the South East), Westwood Cross in Thanet opened in 2005 and delivered a sizeable blow to the nearby town centres of Ramsgate, Margate and Broadstairs.

Meanwhile, Ashford's Designer Outlet opened in 2000 presenting, for many, a rather more attractive alternative to the nearby town centre.

Canterbury's Whitefriars, Maidstone's Fremlin Walk and Folkestone's Bouverie Place all opened in town centres and sought to lure shoppers back in. In Ashford, its County Square, formerly the Tufton Centre, doubled in size in 2007 with a huge glass-fronted expansion.

They all relied heavily on big 'anchor' stores – the sort of big name retailers which pulled in the crowds and took up lots of floor space. Think Marks & Spencers, Debenhams and BHS.

Build it, as the misquoted movie line says, and they will come. And they certainly did. For a while.

But in the time it had taken them to open, so the biggest threat they were to face had started to take hold. The internet's emergence in the last years of the 20th Century may have come with a mistrust of any form of financial transaction online, but the potential was there for all to see.

Tremors were felt when supermarkets moved out of town. Now, the tectonic plates were to shift in the most devastating way possible.

By the time the doors opened on the revamped town centre sites mentioned above, cyberspace was proving a compelling counter case.

In addition, in 2006 a report by the All Parliamentary Small Shops Group – comprising of, as the name suggests, cross-bench MPs – warned that our town centres were at risk of all becoming clones, each hub boasting the same retail chains and nothing to differentiate them.

They warned that, by 2015, independent traders would have largely disappeared.

Said the report of the retail environment at the time: "Witnesses cite the aggression of larger competitors, distortion of the supply chain, the cost of property, crime, poor planning decisions, a lack of appropriate business support and disproportional regulatory burdens as problematic."

Philip Hollobone, a Tory MP on the group, warned: "If nothing is done, British high streets face a catastrophe for independent retailers within 10 years."

What he cannot have imagined, is that add another five years on and many of the biggest chains would have bitten the dust too.

Drained already of many big names, and feeling the impact of online sales, retailers then were hit full in the face, in 2008, by the deepest recession in the UK since the Second World War.

The consequence of the job insecurity it ushered in during its four-year duration? A collective tightening of belts. Why head to the high street and pay for parking when if we wanted something in those straitened times we could go online and, almost inevitably, buy it cheaper?

It was in the second half of 2008 that we were all given a glimpse of what was to come.

Woolworths, the darling of the high street with its eclectic mix of anything and everything (sprinkled with pick 'n' mix) started to struggle and, by the end of the year was heading for collapse. As surprising as its troubles was the lack of appetite to rescue it or take it over.

Faltering under the weight of all the pressures felt in our town centres, and coupled with its expansive stores in key locations commanding the highest rents, it fell over and died in early 2009.

It left huge gaps in almost every major high street. It would not be the last.

During the recession, even the big out-of-town supermarkets felt the pinch. Ironic as their growth was a key contributory factor to the demise of Woolies.

As we left the recession behind during the 2010s, they found themselves rivalled by a new breed of budget retails such as Aldi and Lidl which muscled in on their territory. The recession also saw us become more savvy shoppers – and start turning our back on the weekly shop, preferring instead collecting only what we needed when we needed it.

High streets though, once home to the clichéd butcher, baker and candlestick maker, were in no real position to fill the gap, primarily because many of those traditional specialists had long been squeezed out by the rise of the supermarkets 20 years earlier.

Instead, supermarkets started heading back to town centres with small stores – the 'express' or 'local' outlets which are now so commonplace.

Any independents hanging on for dear life while remaining loyal to the town centres found themselves under siege once again. For many, it was the final straw.

The picture wasn't much brighter for the big names either. Over recent years we've seen the loss of the likes of BHS, Debenhams, C&A, Comet and, when retail giant Arcadia went into liquidation in 2020, former town centre staples such as Burton, TopShop, Dorothy Perkins and Wallis all went puff too.

Other big names have slimmed down their estate. M&S has pulled out of a host of Kent town centres in recent years, most recently, Maidstone.

Those new in-town shopping complexes suffered too. Reliant on well-known stores and high footfall, the loss of some of the big name retailers blew huge holes in their offering.

Their expansion, with the benefit of hindsight, had proved to be poorly timed.

Eleven years ago, Mary Portas, the self-styled Queen of Shops, was recruited by then-Prime Minister David Cameron to conduct an independent review of our high streets. Her report, published in 2011, was widely applauded.

In it, she said: "I believe that our high streets have reached a crisis point. I believe that unless urgent action is taken much of Britain will lose, irretrievably, something that is fundamental to our society. Something that has real social and economic worth to our communities and that after many years of erosion, neglect and mismanagement, something I felt was destined to disappear forever."

Crucially, she called for reviews of business rates and rents charged by landlords.

Both are key factors in the struggles of big and small retailers alike and have played a large role in the high street's struggles.

Without getting too tangled in the maths, business rates are calculated by the rateable value of the properties in which companies operate. So if you're in a high-rent building, you will pay a lot more.

And those prices rocketed while the sun shone – rising some 50% since the 1990s.

There are several bones of contention from retailers. Primarily, it is that the 'rateable value' of properties is based on figures from 2015 – when town centres were in better health than today (the values are due to be reviewed in 2023).

But, perhaps most significantly, is that the rates are disproportionate for high street traders compared to the big online companies which operate out of huge out-of-town warehouse complexes.

Many want a cut for bricks and mortar retailers – funded by an increase for online firms.

Trying to strike a balance is one the Chancellor is only too aware of.

So where should the finger of blame for the high street's decline point? Landlords? Local authorities? Government? Supermarkets? Bluewater? Amazon?

Well, they've certainly all had a role to play. But fundamentally we need to look a little nearer to home.

Market forces dictate the pace of change and the direction in which it travels. If we, as the consumer, opt to cut out the high street and shop for clothes, books and heaven knows what else, in a supermarket, or online, then we determine the growth areas by our actions. If we all decided to shop in our town centres again, then the situation would change once again. Progress is good in so many ways, but there are always casualties.

And that is the challenge now facing all those with a vested interest in our traditional retail centres. Despite all the challenges, there is much to be optimistic about.

For now, our town centres find themselves in a period of evolution, and the way they emerge in the years to come could usher in a new era of popularity. They will, undoubtedly, look very different, but in a sustainable, exciting way.

Yet there is a certain irony about the direction of travel.

To succeed going forward, the advice seems to be: encourage independent traders in and create the much-mentioned 'experience' for shoppers. In other words, lure people in with restaurants, cafés and cinemas – make it a day out.

The fact high streets used to offer just those key components before all the seismic changes in recent decades, will be lost on few.