More on KentOnline

More on KentOnline

Homeowners whose mortgages directly track the Bank of England base rate will see around £50 per month added to their costs typically, according to industry calculations.

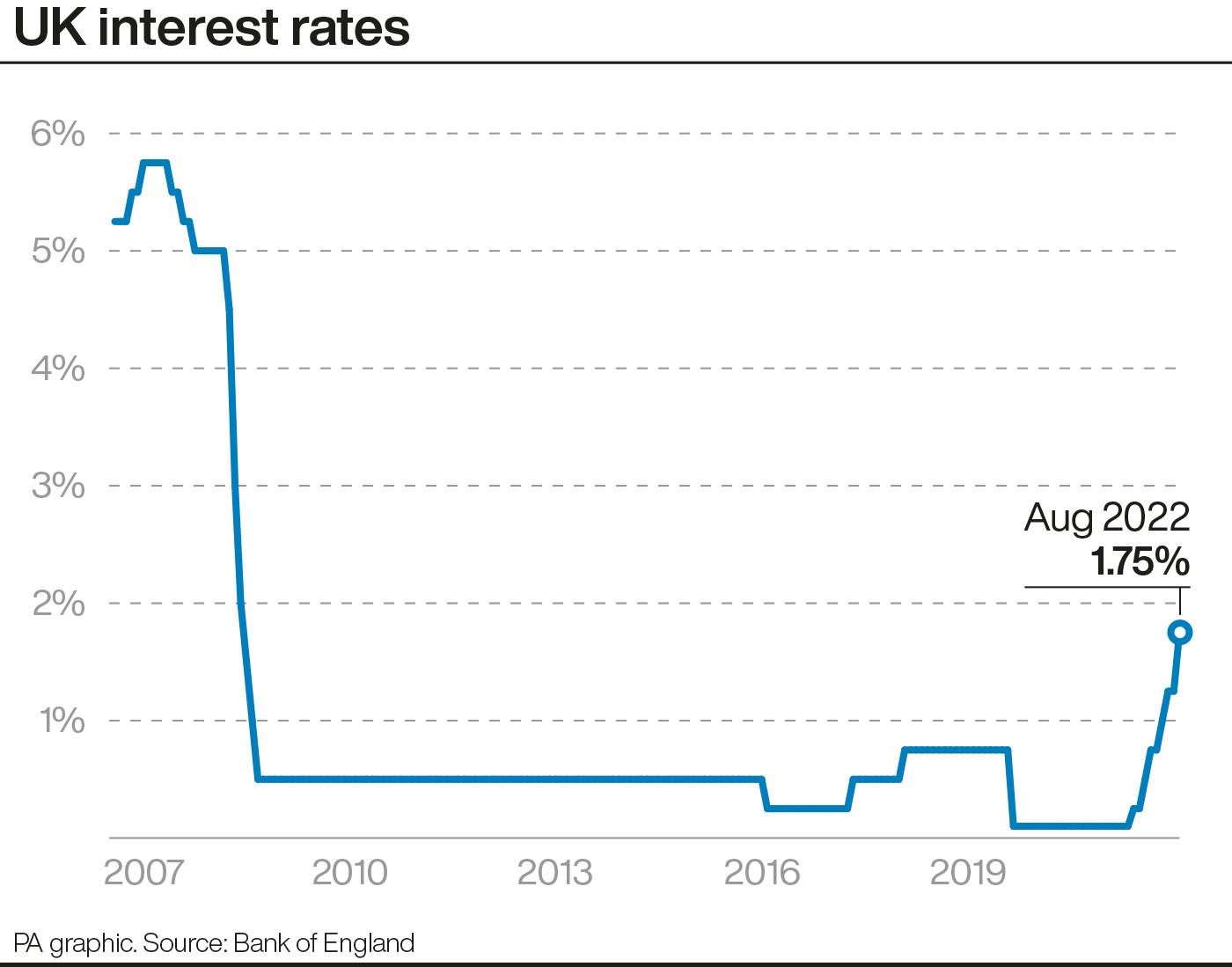

The Bank of England raised the base rate by 0.50 percentage points on Thursday, taking it from 1.25% to 1.75%, marking the biggest single rate jump since 1995.

The £50.43 increase was calculated by trade association UK Finance and is based on average mortgage balances.

This adds up to an extra £605.16 in mortgage costs over the course of a year.

Some homeowners who are nearing the end of their terms are facing a shock when they come to refinance

Simon Gammon, managing partner at Knight Frank Finance, said: “Mortgage rates are now changing on a daily basis and lenders are giving borrowers and brokers little notice about repricing.

“We’re seeing two significant impacts on borrowers. Firstly, some homeowners who are nearing the end of their terms are facing a shock when they come to refinance, because they are unable to borrow as much as they hoped.

“Secondly, those who are looking to buy are realising once obtainable properties are now out of reach.”

There are nearly nine million residential mortgages outstanding, according to UK Finance.

Around three-quarters of these are fixed-rate mortgages, which will not be influenced by changes to the base rate.

Variable-rate deals however may increase as a result of base rate hikes.

Around one in 11 (9%) outstanding mortgages are trackers, while around one in eight (12%) are standard variable rate (SVR) deals.

Borrowers may end up on an SVR when their initial mortgage deal comes to an end. The SVR is set by the individual lender.

Fixing for longer may be in the mindset for some, as there is anticipation for further base rate rises to come

A 0.50 percentage point rise on the current average SVR could add around £1,400 on to a homeowner’s mortgage payments over the next two years, according to Moneyfacts.co.uk.

The calculation is based on a £200,000 mortgage being paid back over 25 years.

The average SVR is currently 5.17%, according to Moneyfacts’ records.

Rachel Springall, a finance expert at Moneyfacts.co.uk, said those sitting on an SVR may find they can save on their mortgage costs by locking into a fixed-rate mortgage.

Based on current average mortgage rates across the market, someone switching from an SVR to a two-year fixed-rate mortgage could save around £3,300 over two years, also based on a £200,000 mortgage repaid over a 25-year term, Ms Springall said.

She continued: “Fixing for longer may be in the mindset for some, as there is anticipation for further base rate rises to come.

“Consumers will find that the average five-year fixed rate has breached 4%, and the rate gap between this and the average 10-year fixed rate has closed in since December 2021.

“The cost-of-living crisis, interest rate rises and house price growth could price out would-be buyers if they have little disposable income and subsequently eat into their savings.

Finding the right combination of rate, fee and criteria will be crucial

“On the other hand, remortgage customers may find they have more equity in their home but will need to get some independent advice on whether they can comfortably afford to switch their deal.”

David Hollingworth, associate director at L&C Mortgages, said he is seeing a growing proportion of borrowers lock into new mortgage rates up to six months before their current rate is due to expire.

He added: “Finding the right combination of rate, fee and criteria will be crucial to find the right option to help manage what will typically be the single biggest outgoing.”

First-time buyers could also find it more of a struggle to get on the property ladder.

Property website Rightmove estimated that new first-time buyers’ monthly mortgage payments could equate to an average of 40% of their gross salary – a level not seen since 2012.

Rightmove said first-time buyers typically face stumping up a deposit of £22,494 for a home, based on current asking prices, compared with £14,316 a decade ago.

Tim Bannister, Rightmove’s housing expert, said: “A new record (average) first-time buyer asking price of £224,943 means that a 10% deposit for a first-time buyer type home is now 57% higher than it was 10 years ago, while average salaries have only increased by 31%.”

Loyal savers meanwhile may not be benefiting from the recent string of base rate rises – and could be missing out on a better return if they fail to compare deals and switch, Moneyfacts said.

The average easy access savings account on the market in August paid 0.69%, having edged up from 0.18% in August 2021.

Easy access Isas meanwhile typically pay 0.76% in interest, up from 0.24% in August 2021.

Ms Springall said: “The patience of some savers may be wearing thin, but there is no guarantee they will see any benefit from a base rate rise. Thankfully, challenger banks and building societies continue to compete in this space.”

Households are coming under mounting pressure from a raft of bill increases – and the Resolution Foundation think tank has warned that inflation could hit 15% in the first quarter of 2023.

The latest base rate rise was announced on the same day that Ofgem confirmed the energy price cap will be updated quarterly, rather than every six months, as it warned that customers face a “very challenging winter ahead”.

Bank of England figures released last week showed that households’ credit card borrowing increased in June at the fastest annual rate since 2005, while the amount of money being deposited into accounts nosedived.

Cost-of-living support, including a £400 discount on energy bills for households plus targeted support for those who are particularly vulnerable, is being rolled out in the months ahead.

Rebecca McDonald, chief economist at the Joseph Rowntree Foundation, said: “Staggeringly high inflation is going to hit low-income families hard.

“We already know seven million low-income families had to sacrifice food, heating, even showers, this year because they couldn’t afford them.

“Many also took on credit to pay their bills and are falling behind on their payments. This will be much harder to pay off with higher interest rates, putting more families in financial peril.”

Robin Fieth, chief executive at the Building Societies Association (BSA), said: “Lenders are sensitive to the rising number of people facing a squeezed household budget.

“Anyone who is worried about their ability to pay their mortgage should get in touch with their lender early and they will do everything possible to help.”