More on KentOnline

More on KentOnline

Bank of England governor Andrew Bailey has insisted controlling rampant inflation is the “absolute priority” as policymakers delivered the biggest hike in interest rates for 27 years and warned over the longest recession since the financial crisis.

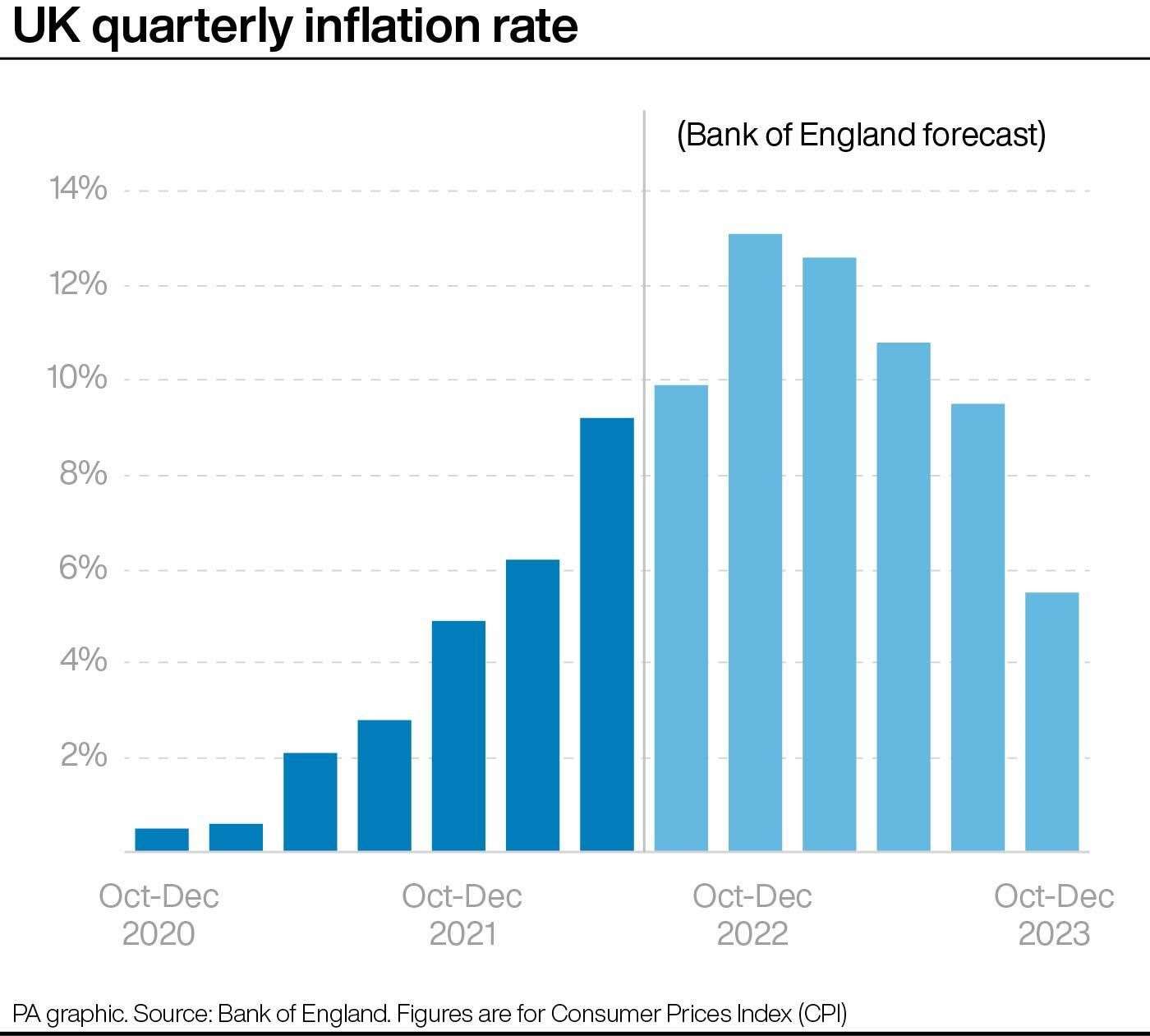

Mr Bailey said there are “no ifs, no buts” over the Bank’s commitment to bringing inflation back to its 2% target as it warned that the Consumer Prices Index (CPI) will hit 13% later this year due to soaring gas prices.

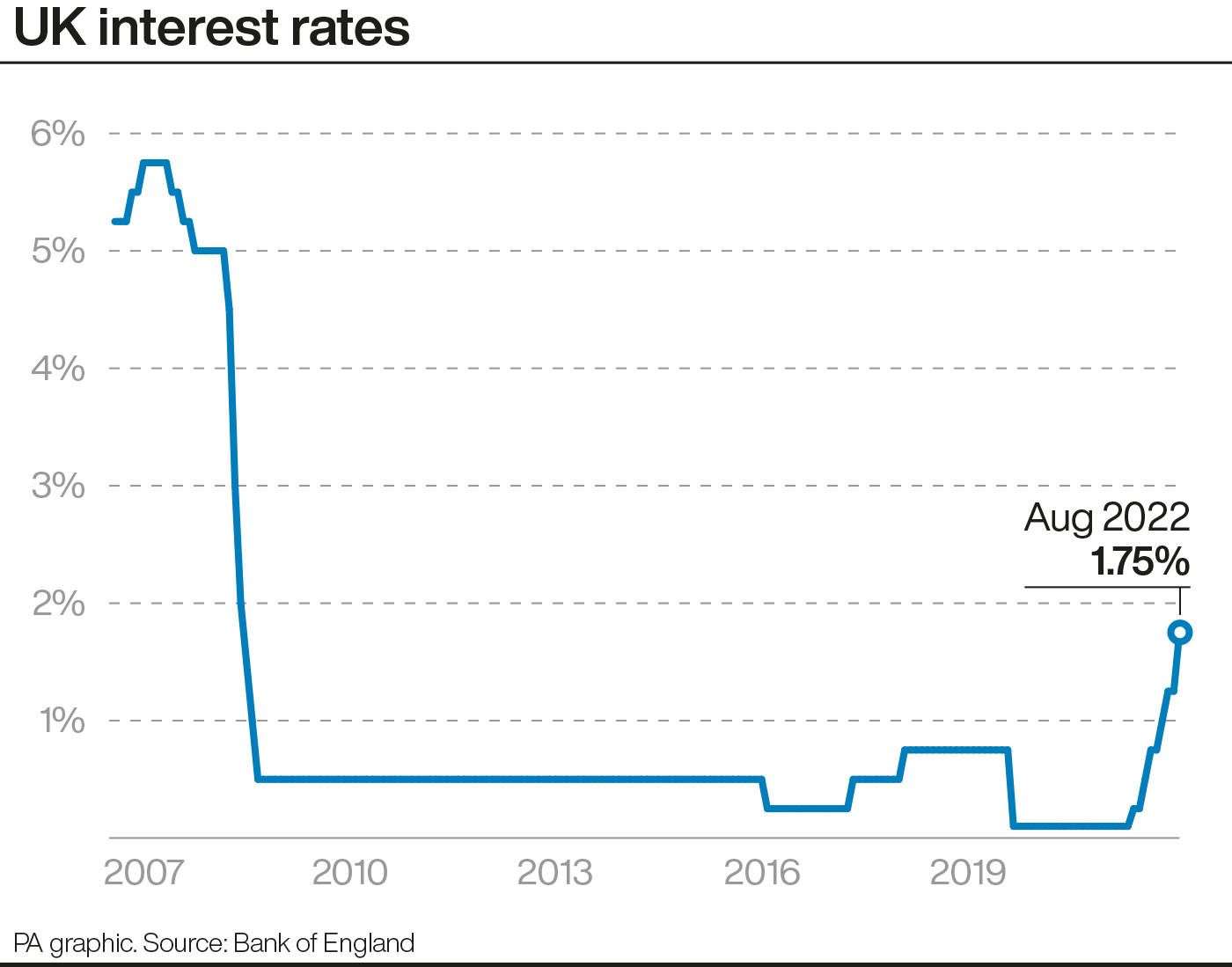

Bank policymakers raised interest rates to 1.75% from 1.25%, the biggest single rise since 1995, as they tried to control the runaway inflation.

Consumer Prices Index (CPI) inflation will hit 13.3% in October, the highest for more than 42 years, if regulator Ofgem hikes the price cap on energy bills to around £3,450, the Bank’s forecasters said.

At a press conference following the rates decision, Mr Bailey said: “Returning inflation to its 2% target remains our absolute priority, no ifs, no buts.”

He said the Bank took “forceful policy action” now to help avoid bigger hikes further down the line.

He said: “I recognise the significant impact this will have, and how difficult the cost-of-living challenge will continue to be for many people in the United Kingdom.

“Inflation hits the least well-off hardest. But if we don’t act now to prevent inflation becoming persistent, the consequences later will be worse, and will require larger increases in interest rates.”

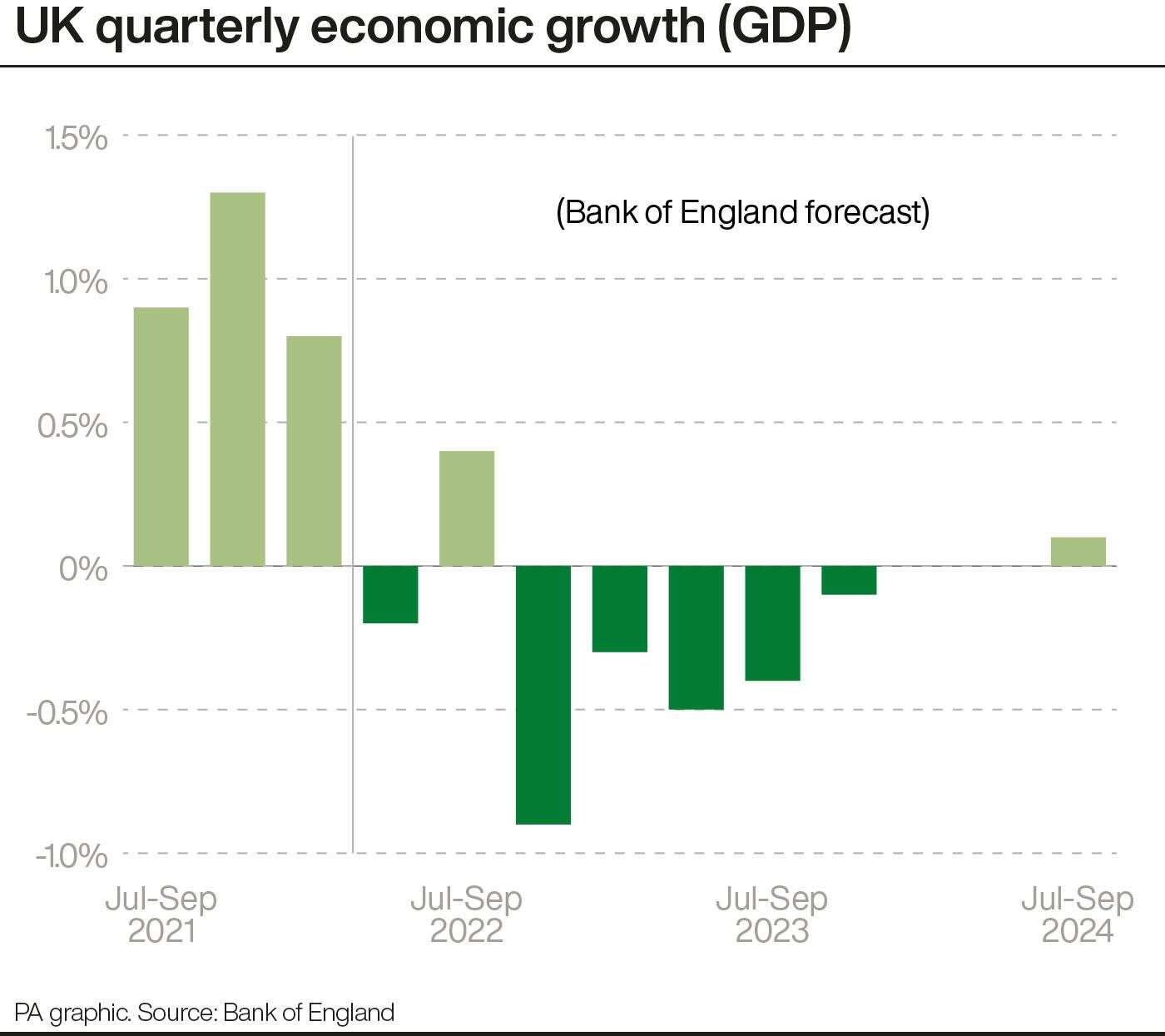

The comments came as the Bank forecast that rocketing energy prices will push the economy into a five-quarter recession – with gross domestic product (GDP) shrinking in the fourth quarter of this year and in each quarter throughout 2023.

The dire economic conditions will see real household incomes drop for two years in a row, the first time this has happened since records began in the 1960s. They will drop by 1.5% this year and 2.25% next.

However, the recession will at least be shallower than the 2008 crash, with GDP dropping up to 2.1% from its highest point.

The Bank said the depth of the drop is more comparable to the recession in the early 1990s.

Mr Bailey said there was an “economic cost to the war” in Ukraine.

“But I have to be clear, it will not deflect us from setting monetary policy to bring inflation back to the 2% target,” he said.

He admitted that the economic outlook for growth and inflation may be even more grim if energy prices rise higher than the current dire predictions.

He said: “Wholesale gas futures prices for the end of this year… have nearly doubled since May,” he said.

They are “almost seven times higher” than forecasts had suggested a year ago, he added.

“That’s overwhelmingly a consequence of Russia’s restriction of gas supplies to Europe and the risk of further cuts.”

The Bank’s latest forecasts show that unemployment will start to rise again next year.

But it expects inflation to come back under control in 2023, dropping below 2% towards the end of the year.

GDP is set to grow by 3.5% this year, the Bank said, revising its previous 3.75% projection downwards. It will then contract 1.5% next year, and a further 0.25% in 2024.

Meanwhile, real post-tax household income will fall 1.5% this year and 2.25% next, it said.

All but one member of the MPC, which sets interest rates, voted for the base rate to rise by 0.5 percentage points to 1.75%.

It puts rates at their highest point since January 2009.