More on KentOnline

More on KentOnline

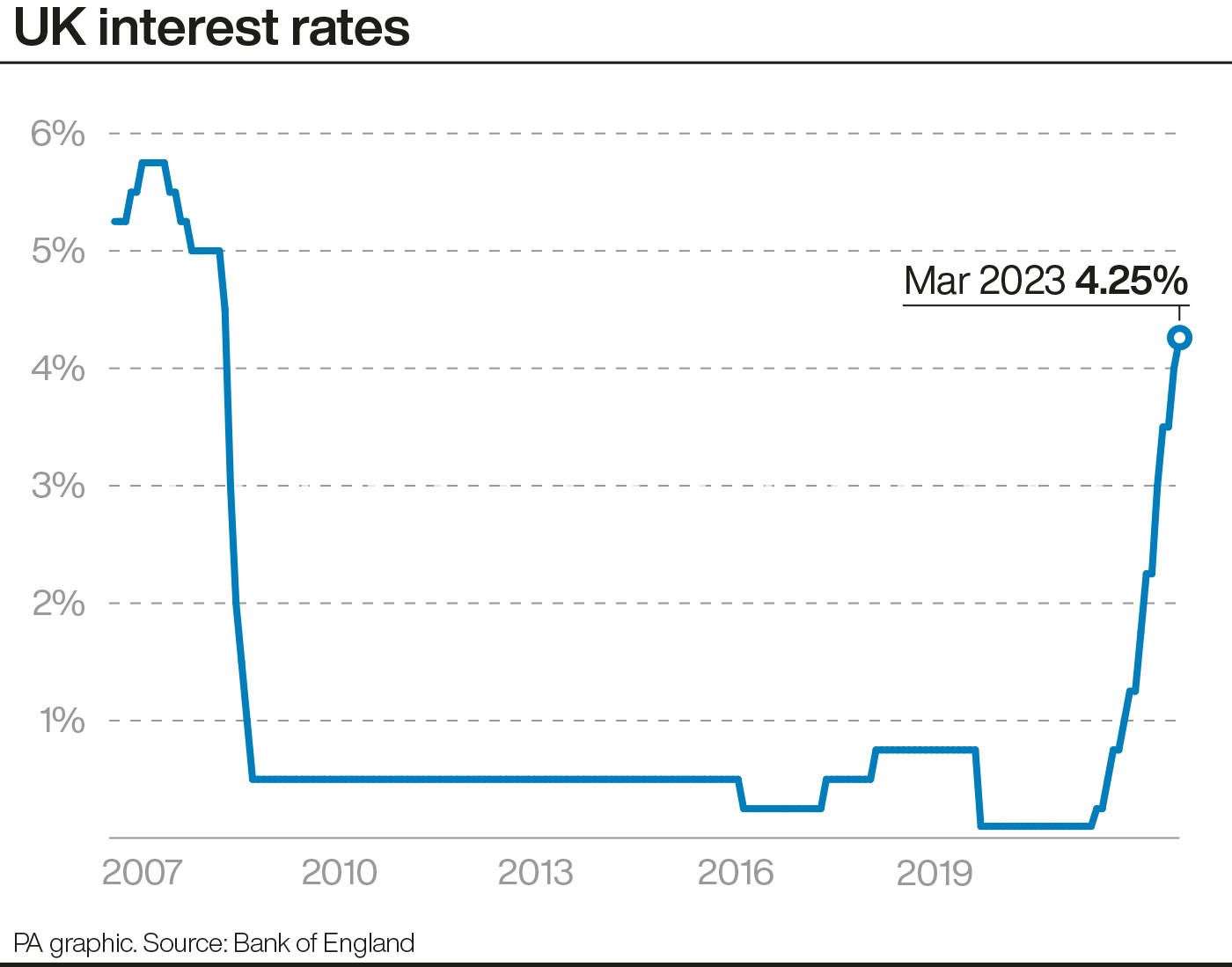

The Bank of England’s boss has said he is more optimistic that the UK can avoid a recession after being on a “knife edge” last month, as it hiked interest rates for the 11th time in a row.

Interest rates were lifted to 4.25% from 4% after policymakers on the Bank’s nine-strong Monetary Policy Committee (MPC) voted seven to two for the quarter point rise following a surprise jump in inflation last month.

But it could be the last in the recent flurry of rises, according to economists.

The Bank gave a surprise upgrade to its forecast for the UK economy, saying it now expects slight growth in the second quarter of the year having anticipated last month it would decline by 0.4%.

It means the country would avoid imminently falling into a recession – which is defined as two consecutive quarters of negative growth.

The Bank’s governor, Andrew Bailey, said: “Back at the beginning of February, we were really a bit on a knife edge as to whether there would be a recession, certainly we thought the economy would be quite stagnant.

“I’m not saying it’s off to the races, let’s be clear, but I am a bit more optimistic,” he said.

Meanwhile, Chancellor Jeremy Hunt said he supports the Bank’s decision to hike rates further as “the sooner we grip inflation the better for everyone.”

Consumer Prices Index (CPI) inflation jumped unexpectedly last month, to 10.4% from 10.1% in January, prompting economists to expect the Bank to raise rates again in a bid to put a lid on inflation.

But the decision was complicated by the recent volatility in financial markets on concerns over a crisis in the banking sector, sparked by the demise of Credit Suisse and the collapse of the US’s Silicon Valley Bank.

The move to raise rates suggested the Bank was prioritising its fight to control inflation over the financial market woes, following similar action by the European Central Bank and the US Federal Reserve in recent days.

However, the MPC said CPI is “likely to fall sharply over the rest of the year”.

It now expects inflation to fall “significantly” between April and June this year, to a lower rate than had been anticipated in the February report.

Falling energy prices could help bring down inflation by about one percentage point over the second quarter, as households continue to benefit from the Government’s Energy Price Guarantee which caps bills at £2,500 for the typical household.

The Bank stood by its view that it would raise interest rates further if it saw evidence of more persistent inflation pressures.

But economists think that Thursday’s rate hike – the 11th it has pushed through in a row since December 2021 – could be the last before rates begin to fall back down.

Experts at Pantheon Macroeconomics said: “As in February’s minutes, the MPC no longer has a presumption of further rate increases, and while we can’t rule out one final 0.25 percentage point hike, we think the committee likely will be reassured sufficiently by inflation developments over the next seven weeks to keep the bank rate on hold at its next meeting in May.”

The pound moved higher after the Bank delivered its decision, lifting 0.5% to 1.232 dollars, suggesting traders were placated by the rate hike.

Meanwhile, the FTSE 100 remained firmly lower after the update, with banks helping to drag it down by about 0.8%.

Business group CBI pointed out that the MPC will need to “have an eye on recent turmoil in the banking sector”.

Anna Leach, CBI’s deputy chief economist, said: “While financial stability is the remit of the Financial Policy Committee, an excessive tightening in credit conditions for businesses and households arising from financial market turbulence could cause the MPC to reconsider the level of interest rates in future months.”

nline

nline