More on KentOnline

More on KentOnline

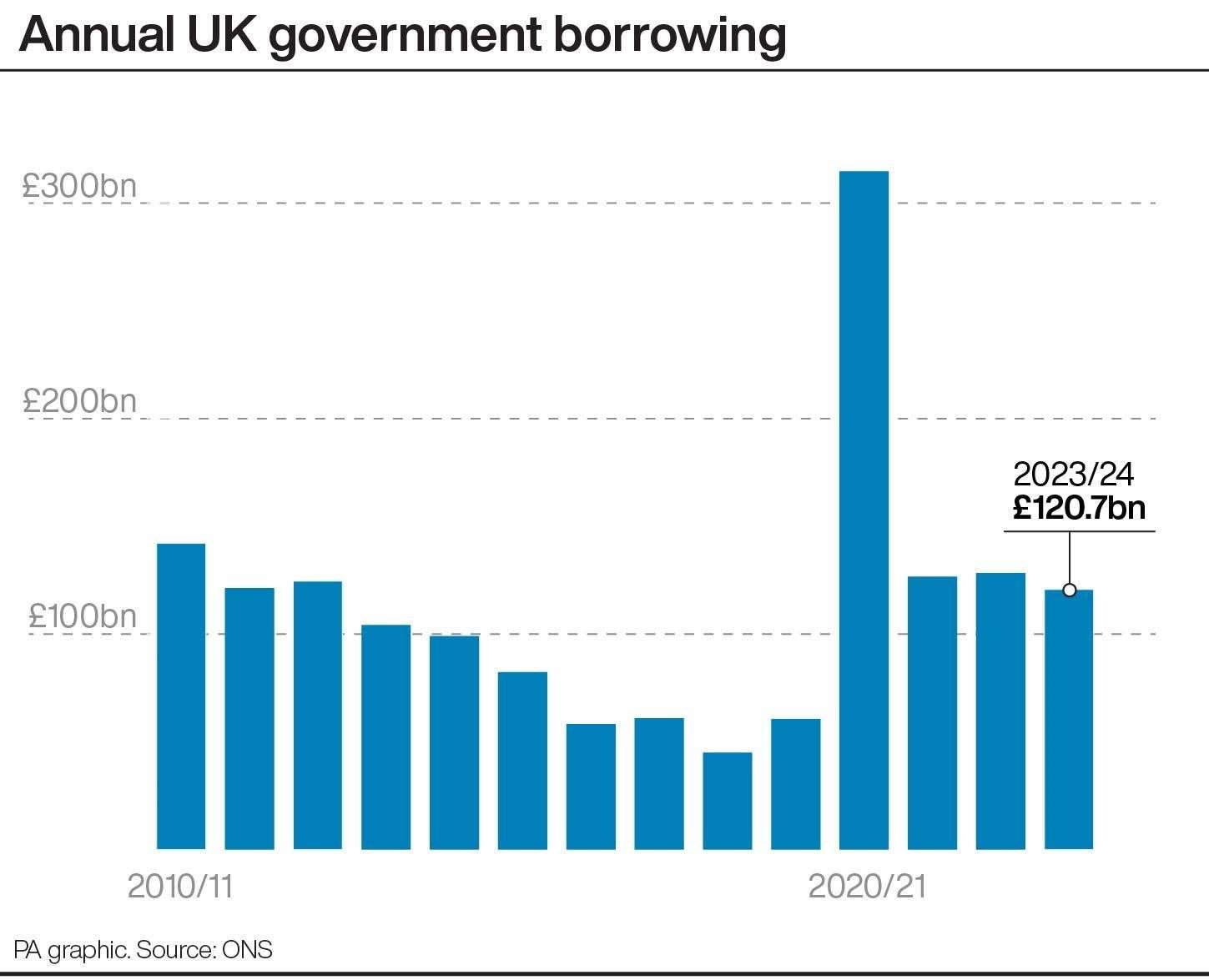

Chancellor Jeremy Hunt has been dealt a blow after official figures revealed borrowing for the last financial year overshot forecasts, hitting £120.7 billion as wages and benefit payments soared.

The Office for National Statistics (ONS) estimated that full-year public sector net borrowing was £7.6 billion less than in 2022-23, but £6.6 billion more than predicted by the UK’s official forecaster.

The Office for Budget Responsibility (OBR) had forecast borrowing of £114.1 billion in the year to the end of March.

It comes after borrowing of £11.9 billion in March, which is £4.7 billion less than a year ago, but higher than the £10 billion expected by most economists.

Jessica Barnaby, ONS deputy director for public sector finances said: “Spending was up about £58 billion, with increased spending on public services and benefits outstripping large reductions in interest payable and energy support scheme costs.”

The higher-than-predicted figures are seen as limiting the scope of any tax giveaways by the Chancellor ahead of the general election.

But some experts believe the figures will not stop Mr Hunt from looking to cut taxes later this year to boost election chances.

Andrew Goodwin, senior economic adviser to the EY Item Club, said: “Unless the Chancellor is prepared to assume even greater spending restraint, it’s unlikely there will be another tax-cutting fiscal event before the election.”

However, Rob Wood at Pantheon Macroeconomics said: “We expect the Chancellor to cut taxes again before a likely October or November general election, despite borrowing overshooting his forecasts.”

He added: “Hunt can plan for another year of unrealistically weak public spending to generate ‘headroom’ against his fiscal rules and thereby manufacture the funds to cut taxes.

“The next government will, therefore, face a tricky choice between raising taxes to fix creaking public services or holding the line on the Chancellor’s recent tax cuts.”

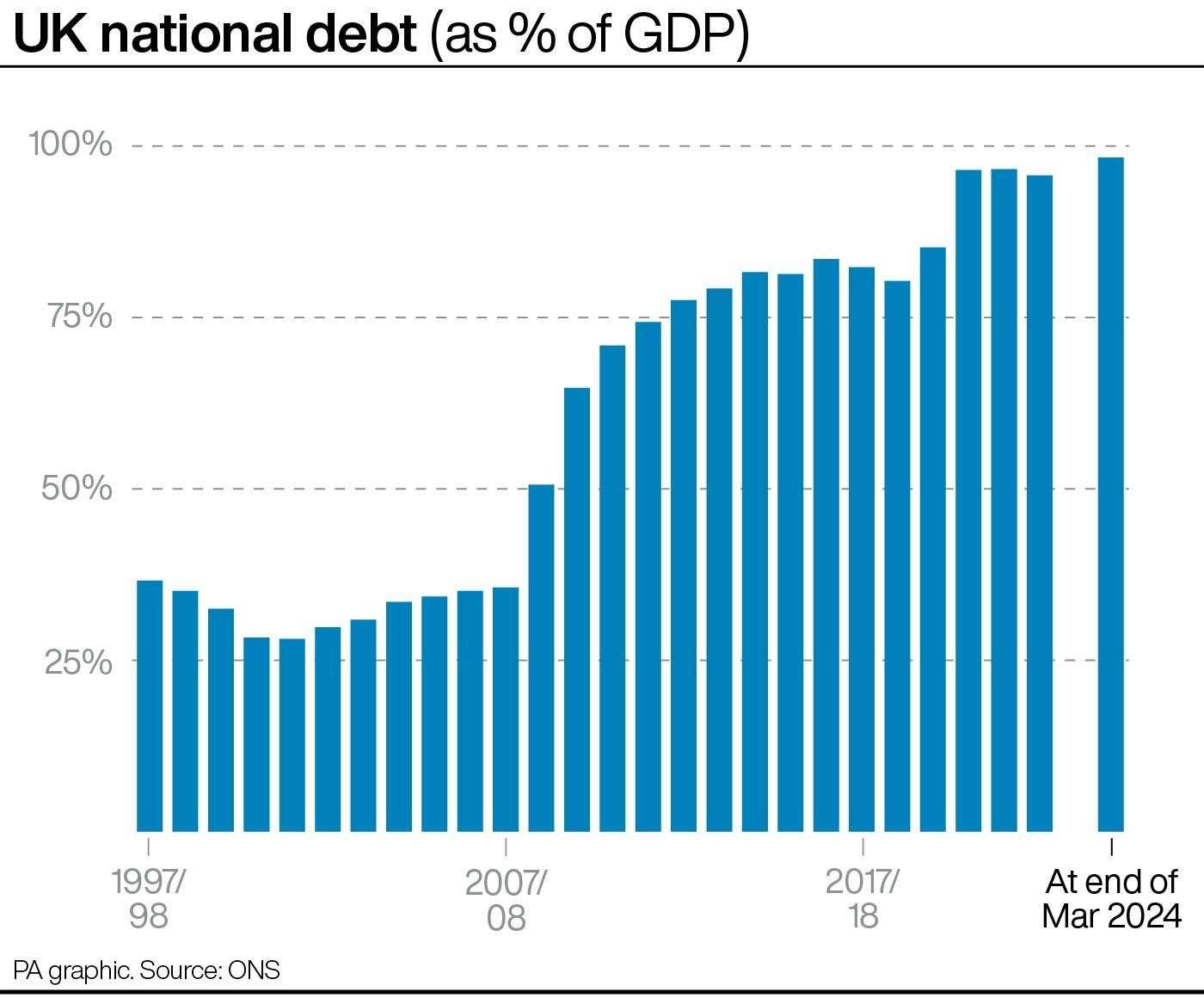

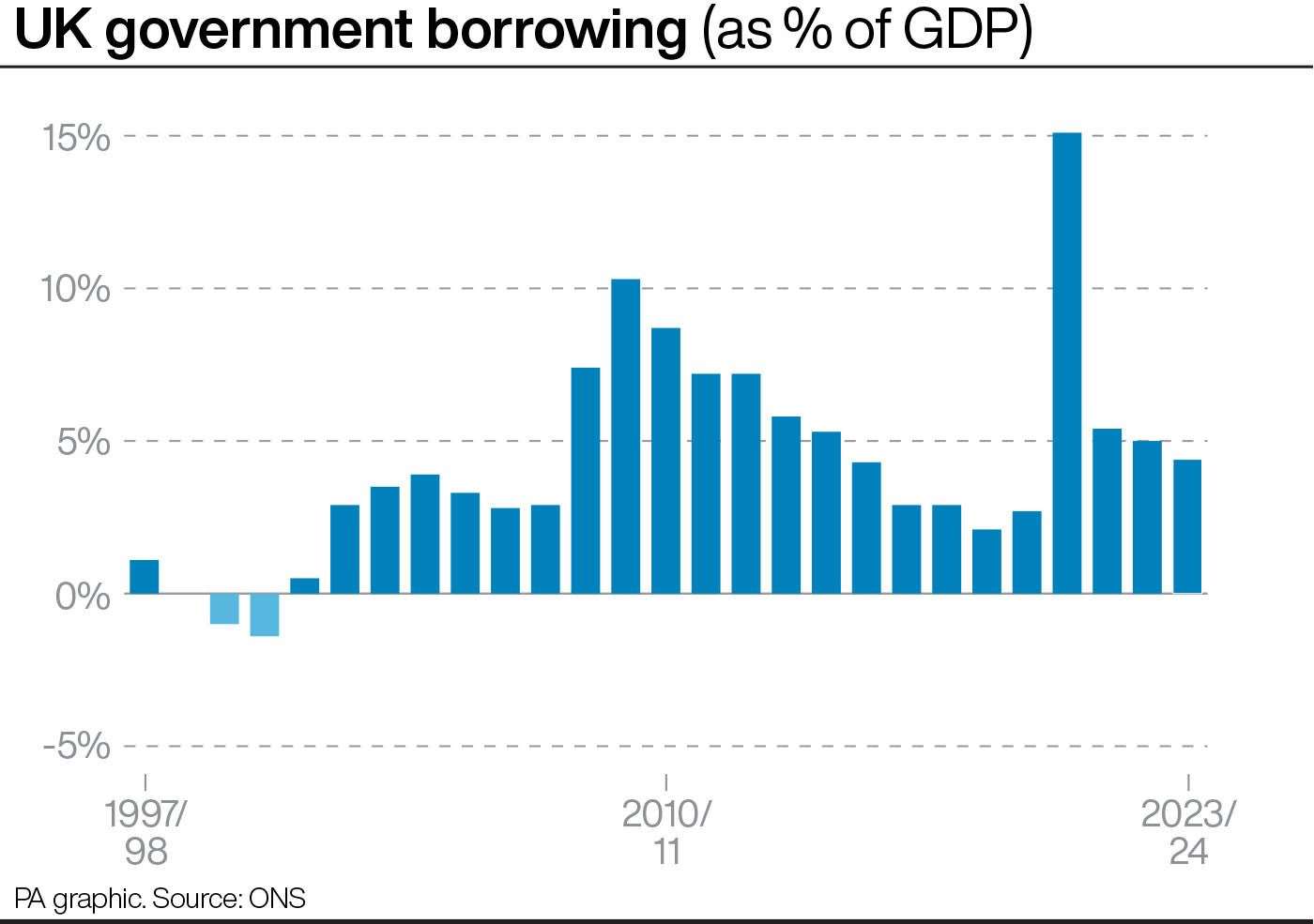

Overall, the figures show the UK’s overall national debt was £2.69 trillion in March, an increase on the £2.54 trillion seen a year ago.

As a share of the economy, debt was around 98.3% of the UK’s annual gross domestic product (GDP) in March, around 2.6 percentage higher than a year earlier and remaining at levels last seen in the early 1960s, the ONS said.

A spokesman for the Treasury said: “Debt increased in recent years because we rightly protected millions of jobs during Covid and paid half of people’s energy bills after (Vladimir) Putin’s invasion of Ukraine sent bills skyrocketing.”

He added the Government “must stick to the plan to get debt falling”.

The figures show the impact of inflation, with benefit payments surging by £36.9 billion to £291.4 billion in the year, as payouts saw inflation-linked increased and due to cost of living support.

Central government wages also rose by £21 billion, including across health and education, while goods and services also cost the Government more.

But there was some relief as inflation eased back from the highs seen in October 2022, which helped interest on inflation-linked debt fall 27% to £78.3 billion over the year.

In March, borrowing debt interest increased by a fifth to £2.5 billion, due to changes in Retail Prices Index inflation.

But borrowing overall is still lower than the previous year, which was pushed up by energy support payments after Russia’s war with Ukraine sent gas and electricity costs soaring.