More on KentOnline

More on KentOnline

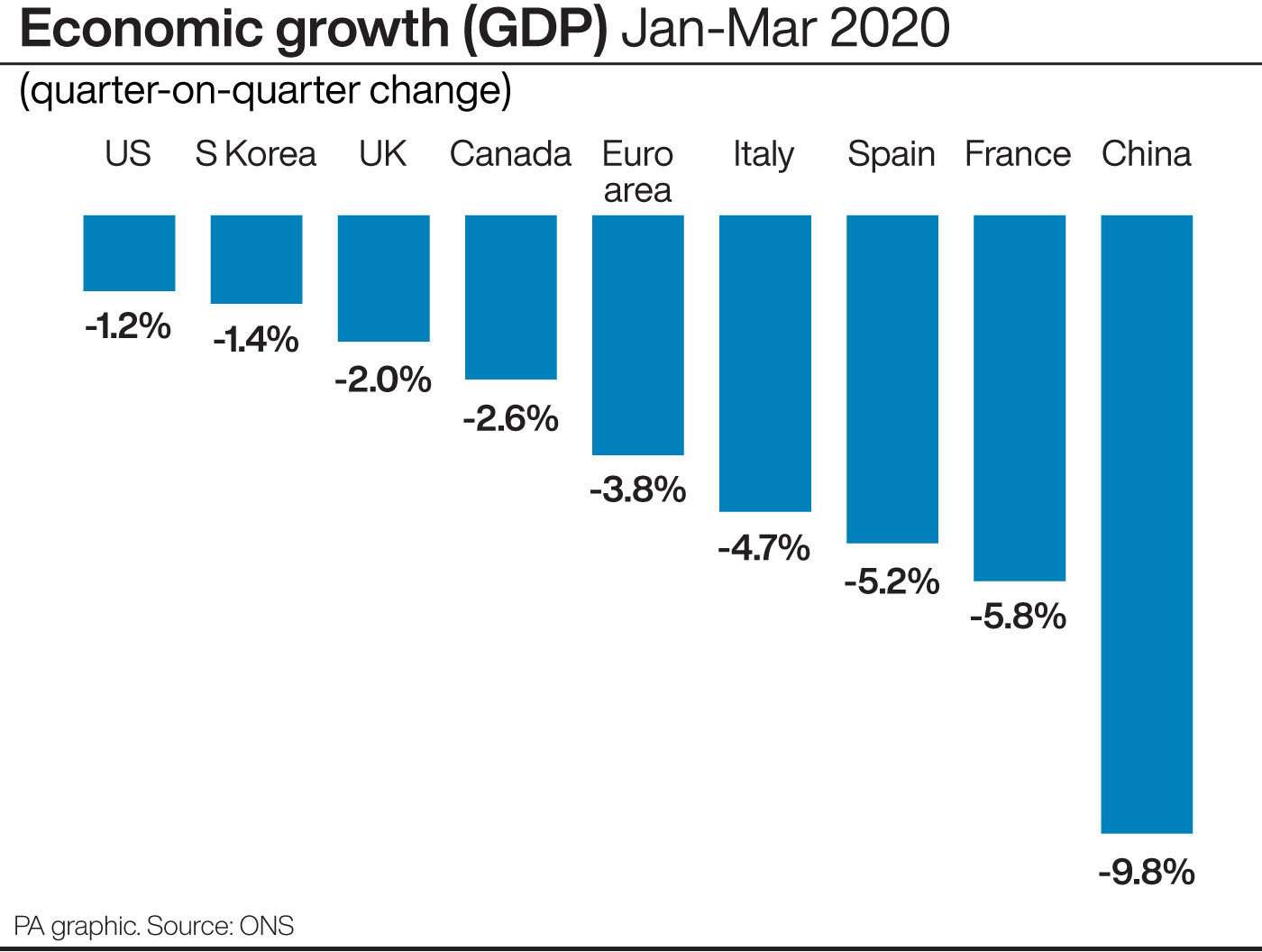

The UK economy contracted at the fastest pace on record in March as the coronavirus crisis puts Britain on the brink of the worst recession in 300 years.

The Office for National Statistics (ONS) revealed activity plunged 5.8% in March in the biggest monthly fall since records began in 1997.

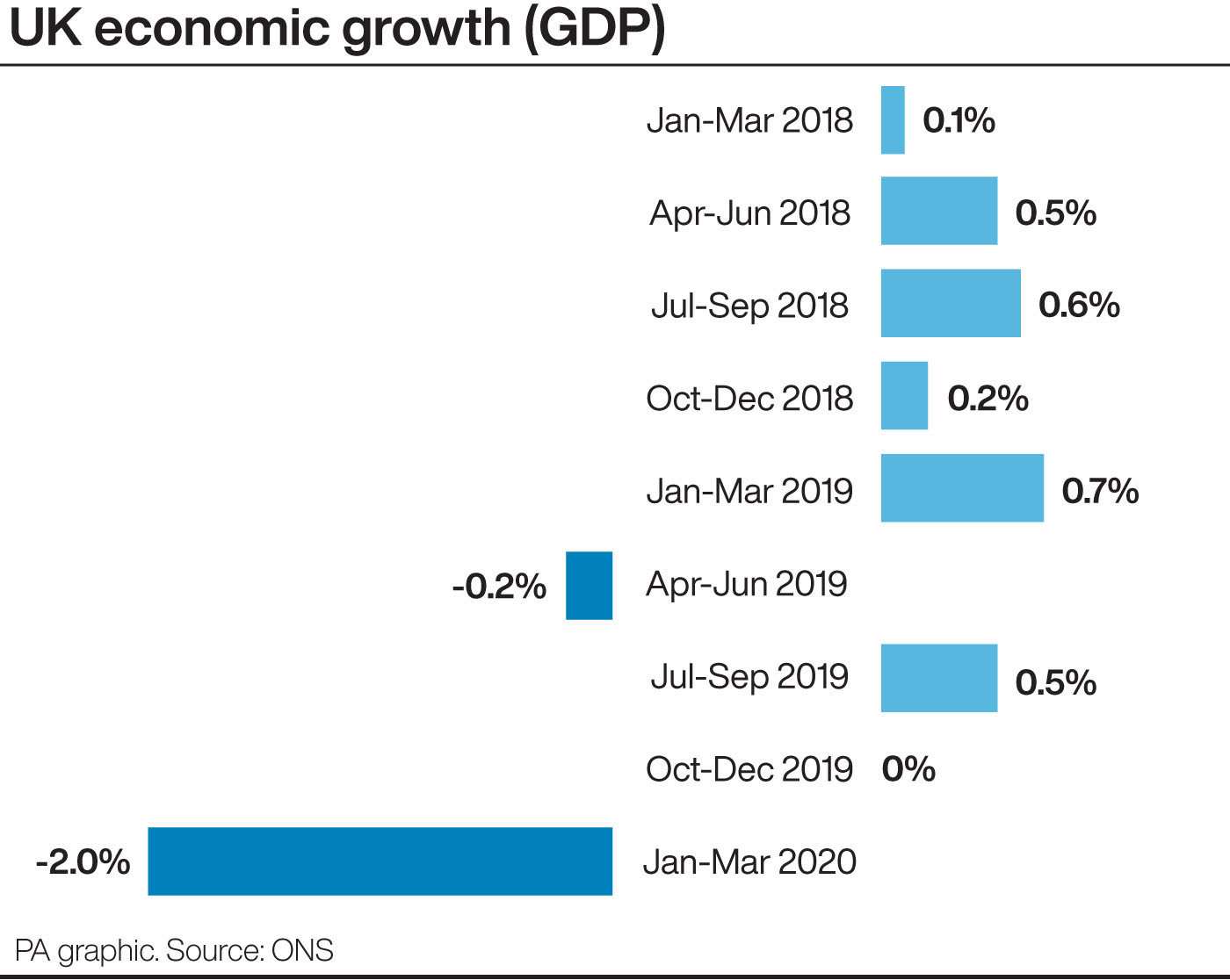

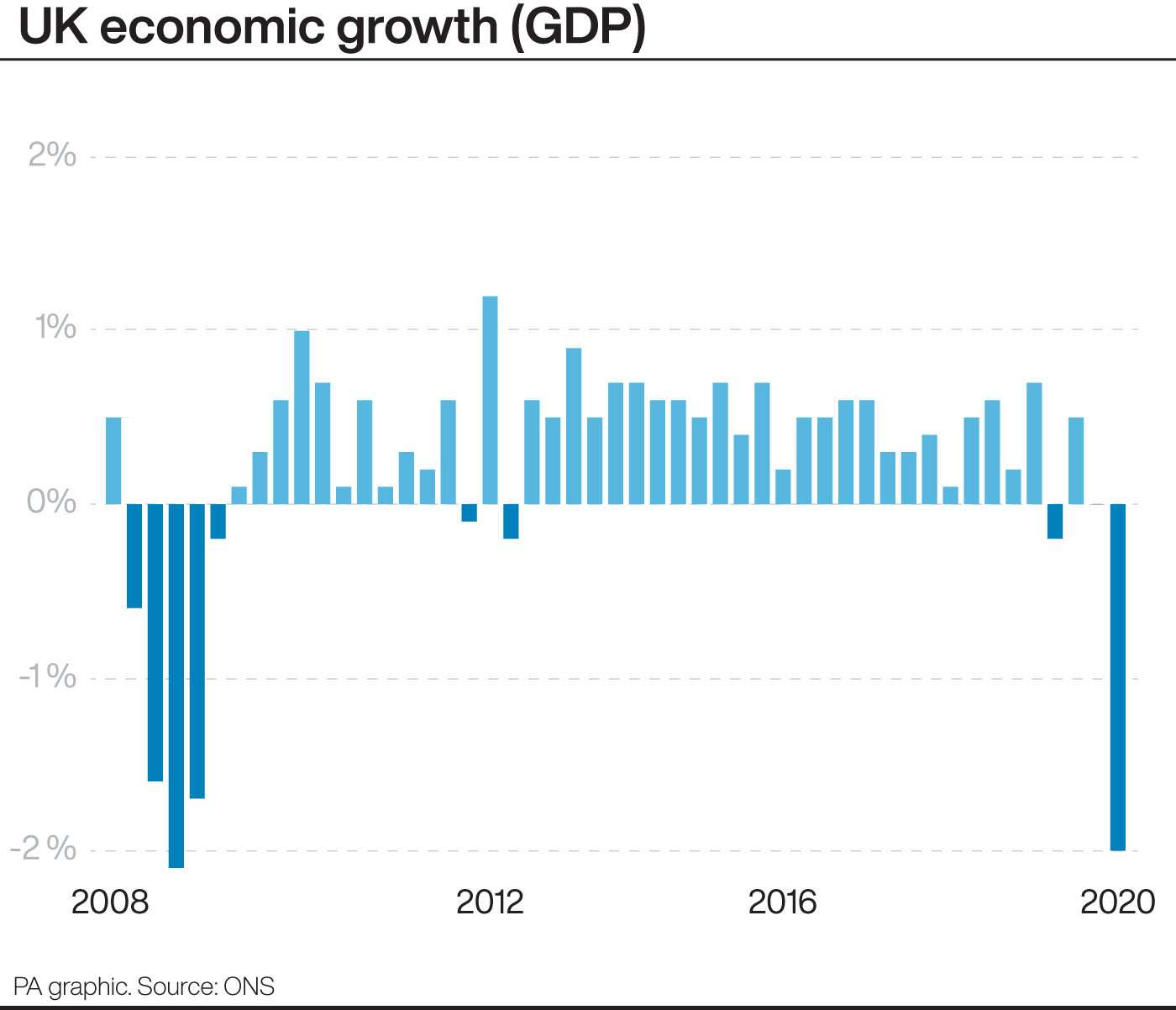

The March tumble sent gross domestic product (GDP) down 2% overall in the first quarter – the biggest fall since the end of 2008 when Britain was at the height of the financial crisis.

The latest figures show the first direct effect of the Covid-19 pandemic on the UK economy after the country was placed in lockdown to control the spread of the virus.

But with the lockdown only coming into place on March 23, the second quarter will show the full hit on the economy after the UK ground to a standstill.

Experts said the first quarter data suggested the economy could contract by up to 20% between April and June as the full effects of the lockdown are captured.

The Bank of England last week warned coronavirus could see the economy plunge by as much as 25% in the second quarter and fall by 14% overall in 2020 – the worst annual fall for more than three centuries.

London’s FTSE 100 Index fell 1.3% after the GDP data and amid concerns over a second wave of coronavirus cases in countries that have started to reopen post-lockdown.

Chancellor Rishi Sunak has said it is “very likely” that the UK will face a “significant recession” as a result of the coronavirus crisis.

He told the BBC: “A recession is defined technically as two quarters of decline in GDP.

“We’ve seen one here with only a few days of impact from the virus, so it is now very likely that the UK economy will face a significant recession this year and we are in the middle of that as we speak.”

The Institute of Directors said the official data was a”sobering first glimpse of the economic turmoil caused by the outbreak”.

George Brown, at Investec Economics, added: “While the figures look ugly today, they are just the tip of the iceberg.”

There are hopes the fall-out may be helped by the Government’s move to begin lifting some of the lockdown restrictions on Wednesday and its decision on Tuesday to extend the crucial furlough scheme for workers until October.

But the economy is expected to bear some long-lasting scars of the crisis.

James Smith, at ING, said the economy could take two years to recover.

“The prospects of a ‘V-shape’ recovery have long since faded, and we don’t expect the size of the UK economy to return to pre-virus levels until at least 2022,” he said.

The ONS figures showed all sectors were hammered in the first quarter, with a 1.9% drop in services output marking the largest quarterly fall on record.

Production output also fell by 2.1% in the first quarter, driven by declines in manufacturing, while construction output dropped by 2.6%.

The first quarter contraction comes after already weak growth at the end of 2019, when GDP was flat in the fourth quarter.

Trade data also showed the UK deficit widened to a far higher-than-expected £6.7 billion in March from £1.5 billion in February, with the ONS saying UK imports and exports fell over the last couple of months, including a notable drop in imports from China.

But the ONS cautioned there was more uncertainty than normal over its figures, given the challenges of collecting economic data amid the lockdown.

nline

nline