More on KentOnline

More on KentOnline

Bank of England deputy governor Ben Broadbent has warned Britain is likely to be facing the worst ever external hit to national income from inflation as the Ukraine war compounds the cost-of- living crisis.

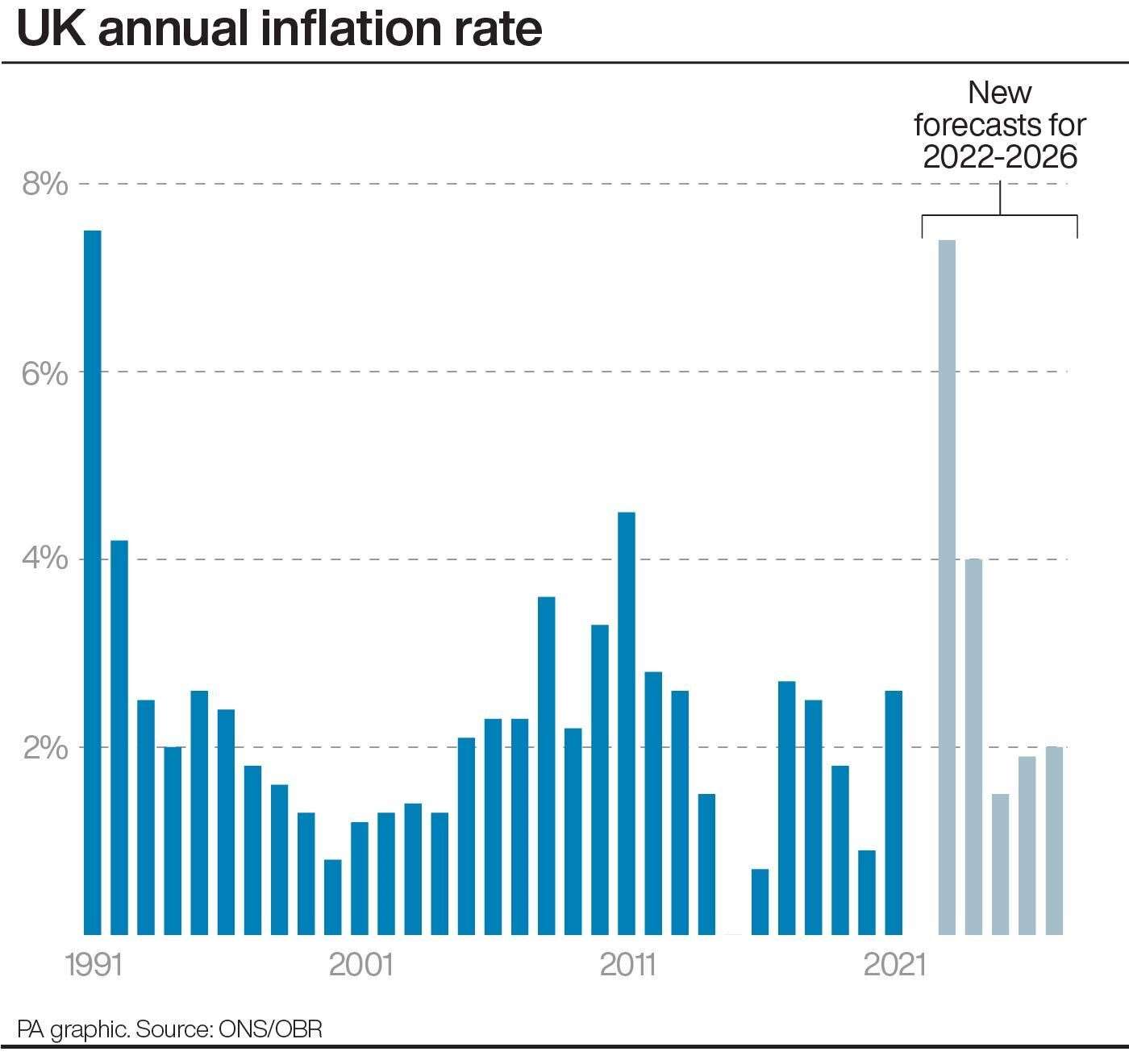

In a speech in London, Mr Broadbent – who sits on the bank’s interest rate setting committee – said the scale of the impact is potentially unprecedented as the UK braces for inflation to hit a 40-year high of nearly 9%.

He said: “As a big net importer of manufactures and commodities, it’s doubtful that the UK has ever experienced an external hit to real national income on this scale.

“From the narrow perspective of monetary policy it will result in the near term in the difficult combination of even higher inflation but weaker domestic demand and output growth.”

It comes after the Office for Budget Responsibility (OBR) last week said households will suffer the biggest fall in incomes since records began in 1956 as it forecast inflation would peak at 8.7% in October.

The Government’s fiscal forecasters slashed its growth outlook for the UK economy this year and next, to 3.8% in 2022 and 1.8% in 2023, due to the impact of rocketing inflation.

The bank raised rates at its third meeting in a row earlier this month, to 0.75%, as it also predicted slowing growth as cash-strapped households and businesses rein in spending.

Mr Broadbent also used his speech to the National Institute of Economic and Social Research (Niesr) to caution that forward guidance on interest rates must be clear and warned against an over-reliance on policymaker comments.

He said statements about the likely path of rates carry the risk that financial markets do not take enough notice of economic data.

It comes after the Bank of England has been accused of acting like an “unreliable boyfriend” – a tag first used to describe former governor Mark Carney, by failing to raise rates after implying they would go up.

The bank caught markets off guard when it did not raise rates last November as inflation was surging, and some of its policymakers have hinted that forward guidance may be ditched.

Mr Broadbent said: “If people come to rely too much on explicit steers from the central bank, forward interest rates and other asset prices may become insufficiently sensitive to economic events.

“If in turn the central bank acquiesces to the desire for more definitive statements about the future path of interest rates, and feels the need to signal policy changes well in advance, this could compromise its ability to respond to surprises that occur in the meantime.”

nline

nline