More on KentOnline

More on KentOnline

UK interest rates will fall by less than expected over the next two years after the autumn Budget’s significant spending and borrowing plans, according to an influential report.

In its annual economic survey, the Organisation for Economic Co-operation and Development (OECD) said UK inflation will also surpass previous forecasts next year, and upgraded growth projections for the economy, because of a budget boost.

The OECD said the global economy would “remain resilient” over the coming years but that “risks and uncertainties are high”.

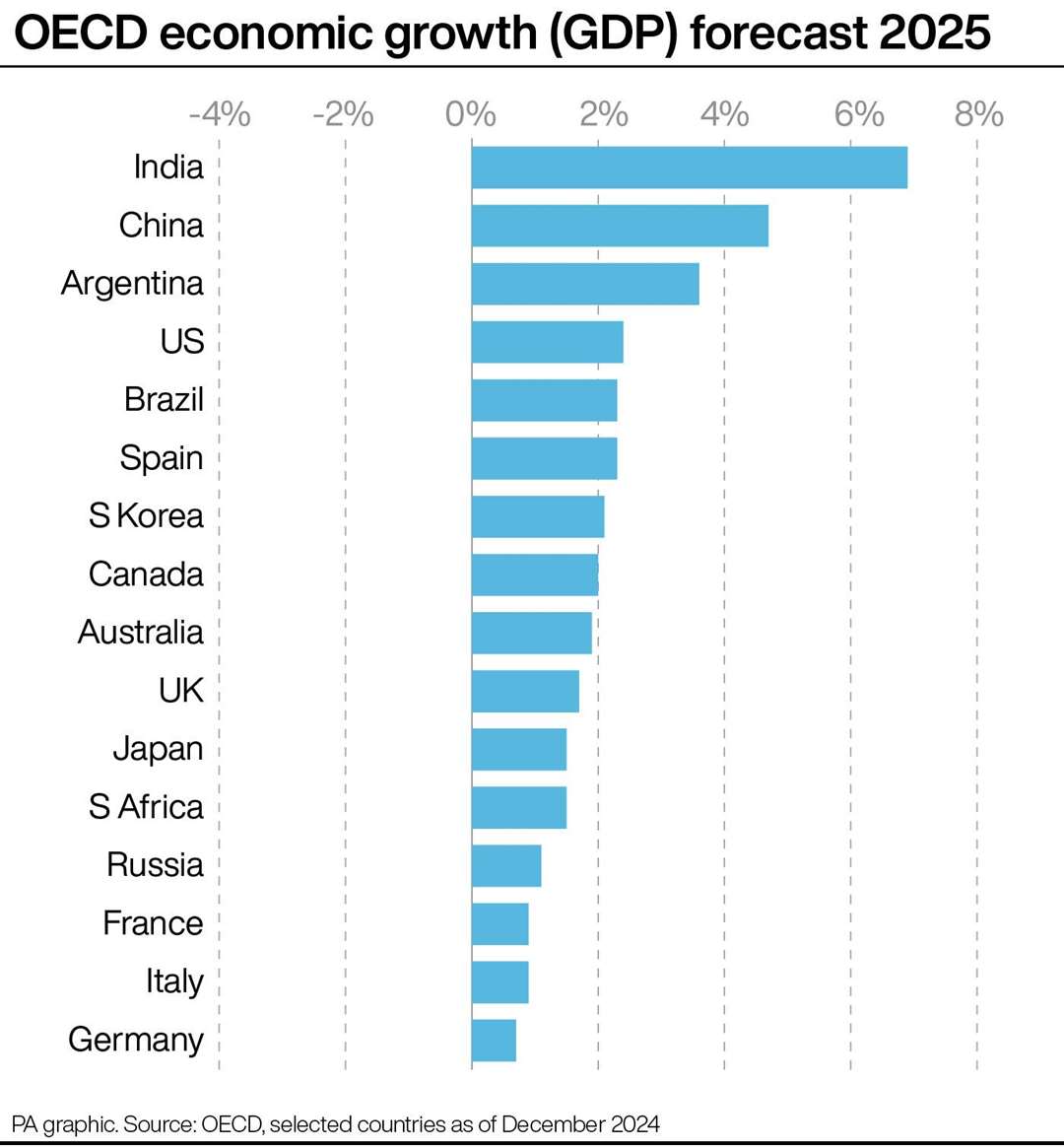

The global economy is predicted to grow by 3.2% this year and 3.3% next year, the organisation said.

It reflects a slight improvement from its predictions of 3.1% and 3.2% respectively, from its September interim report.

Meanwhile, UK gross domestic product (GDP) is predicted to rise by 0.9% this year.

This is a downgrade from its previous 1.1% forecast after recent data from the Office for National Statistics (ONS) showed that the economy only grew by 0.1% in the third quarter of the year.

“But momentum is positive nevertheless, with retail sales on an upward trend since early 2024,” the report added.

It indicated that GDP growth will now strengthen to 1.7% next year as it is “boosted by the large increase in public expenditure set out in the autumn budget”. This will then slow to 1.3% in 2026.

Previously, the OECD had forecast 1.2% GDP growth for next year.

In October, Chancellor Rachel Reeves set out plans for almost £70 billion a year of extra public spending, funded through tax rises and increased borrowing.

The OECD said on Wednesday that interest rates, which currently sit at 4.75%, are expected to fall back to 3.5% by early 2026.

However, it said higher consumption, partly caused by the autumn Budget, meant this is not as sharp a drop as previously forecast.

Growth is our number one priority, and the OECD upgrade will mean the UK is the fastest growing European economy in the G7 over the next three years

The report said: “Fiscal policy will be tightening over 2024-26, though by less than expected, with significant fiscal loosening in the tax, spending, and borrowing package announced at the autumn Budget.”

This is partly linked to higher-than-expected inflation, with the OECD predicting headline inflation of 2.7% for next year.

It had previously pointed towards inflation of 2.4% for the year.

Inflation is then expected to fall to 2.3% in 2026, but will therefore still remain above the Bank of England’s 2% target rate.

Ms Reeves said: “Growth is our number one priority, and the OECD upgrade will mean the UK is the fastest growing European economy in the G7 over the next three years.

“That is only the start. Growth only matters if it’s matched by more money in people’s pockets.

“This Government will get our economy growing, with our National Wealth Fund, reforming the remits of our regulators and pension mega funds to attract better investment, as well as reforming our planning laws – all so that we can rebuild Britain for good.”