More on KentOnline

More on KentOnline

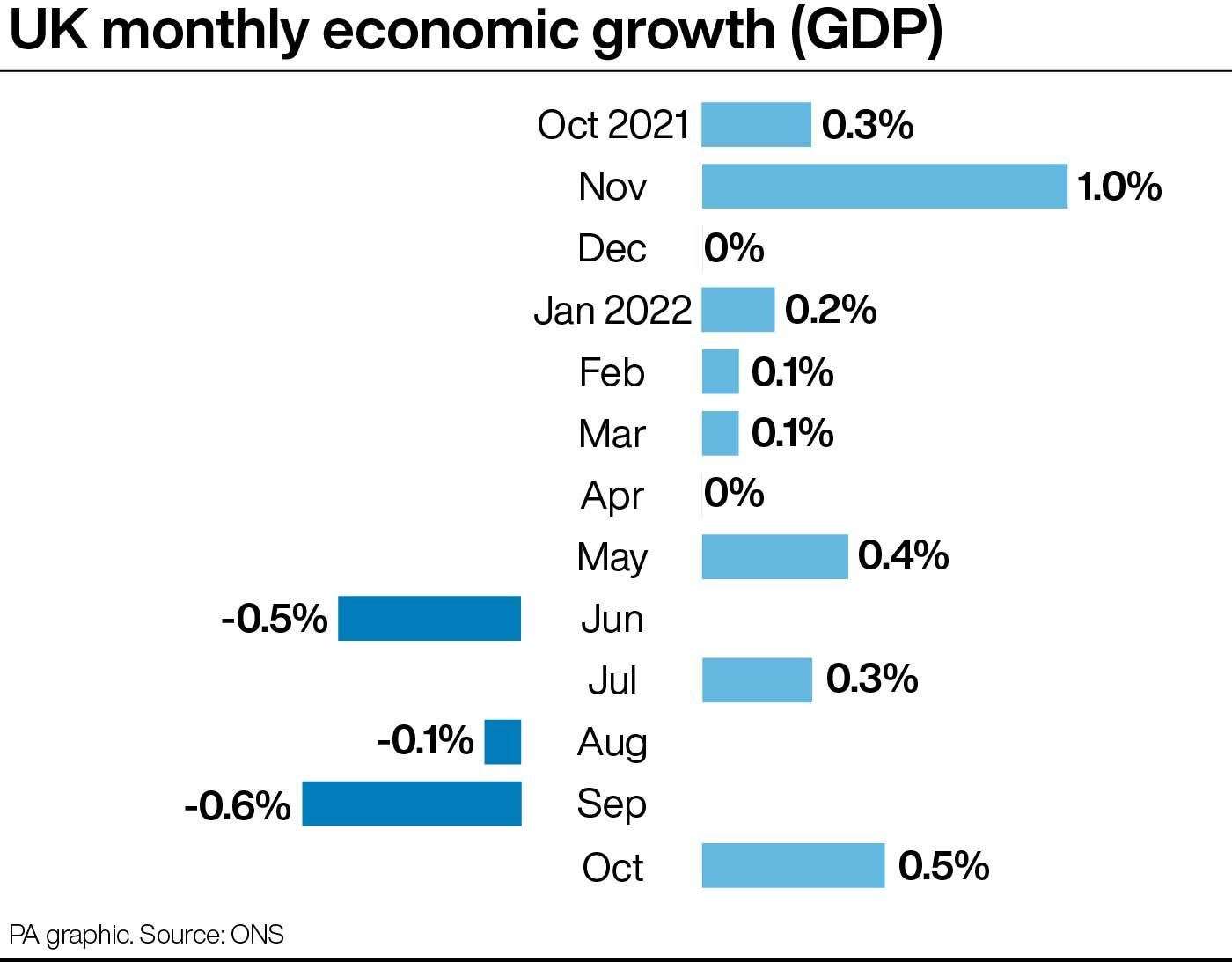

Britain’s economy rebounded in October after output in September was impacted by the extra bank holiday for the Queen’s funeral, but experts said the recovery was a “false dawn” with a recession still on the cards.

The Office for National Statistics (ONS) said gross domestic product (GDP) grew by a better-than-expected 0.5% between September and October in a bounce back from a 0.6% contraction the previous month, which was hampered by fewer working days due to the Queen’s state funeral.

The monthly data masks an underlying worsening picture for the economy, with the less volatile figures for the three months to October showing a 0.3% drop in GDP compared with the previous three months.

Experts said the UK is still on track for a likely recession by the end of the year as the cost-of-living crisis hits demand.

Chancellor Jeremy Hunt warned there was a “tough road ahead”.

He said: “These figures confirm that this is a very challenging economic situation, here and across the world and it will get worse before it gets better.

“But we have a plan that will more than halve inflation over the next year. And if we stay the course, we can get back to the strong economic growth that we need.”

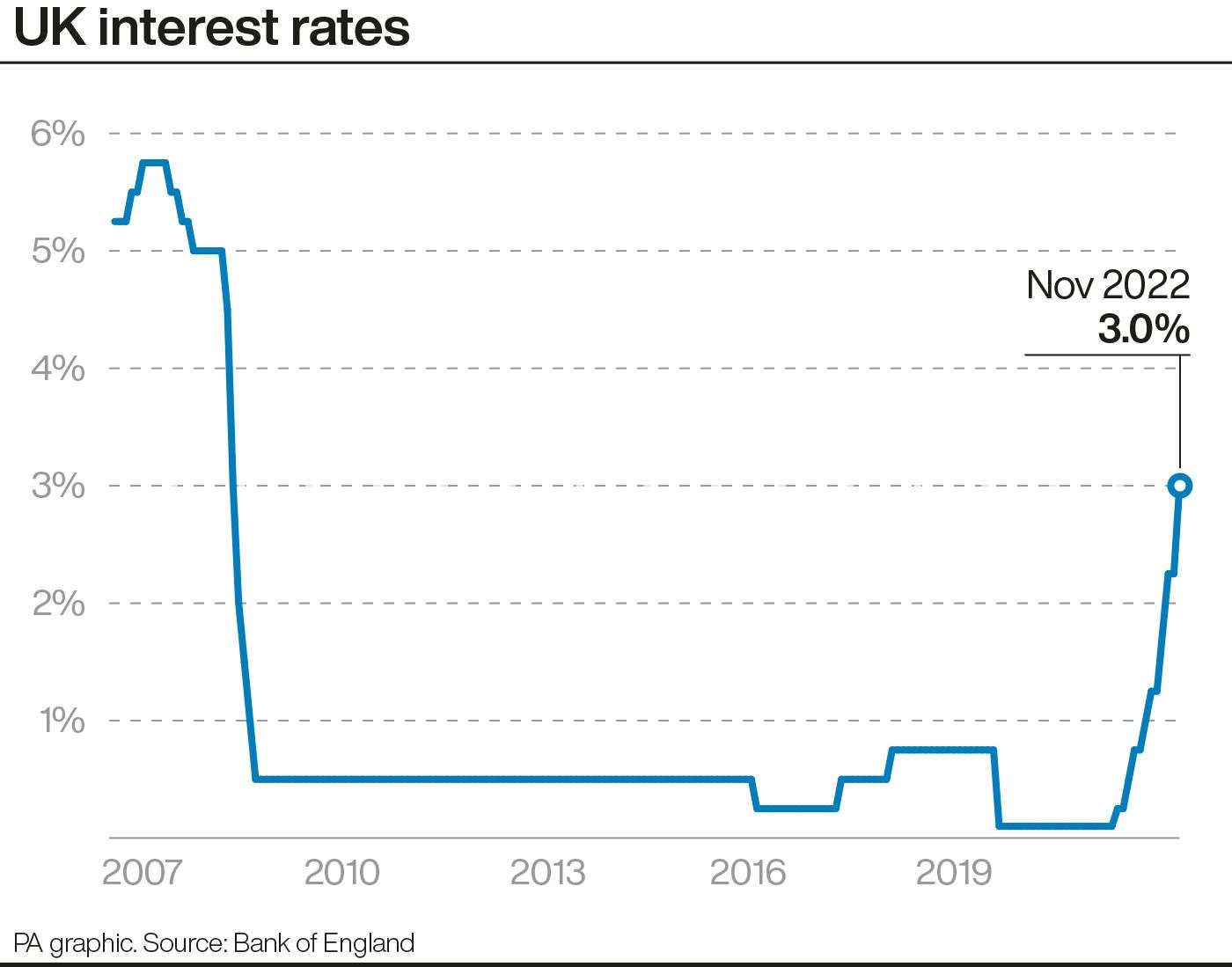

The Bank of England is still battling to rein in sky-high inflation that is weighing on growth, and is set to hike interest rates again on Thursday despite the worsening economic outlook.

Economists are pencilling in a rise from 3% to 3.5% – which would be the highest level for 14 years.

Suren Thiru, economics director at the Institute of Chartered Accountants in England and Wales (ICAEW), said October’s rebound was a “false dawn for the economy”.

He said: “The positive start to the fourth quarter may not prevent recession with the growing squeeze on incomes likely to drive falls in GDP in November and December, despite a possible boost to consumer activity from the World Cup.

“A half-point interest rate rise on Thursday is expected. However, tightening monetary policy too aggressively could risk worsening the financial outlook for firms and households, and extend the looming downturn.”

The ONS figures showed October’s rebound was the biggest expansion since November 2021 and was more than the 0.4% rise expected by most economists.

The services sector – the biggest sector of the economy – expanded by 0.6% in October after a 0.8% drop in September, boosted by a recovery in car sales as well as the health sector due largely to a ramp up in Covid-19 tests and vaccinations amid the autumn booster campaign.

The manufacturing sector rose by 0.7% and construction industry saw 0.8% expansion – the fourth monthly increase in a row.

We continue to expect a peak-to-trough fall in the quarterly measure of GDP of about 2%, and doubt that the economy will grow again until early 2024, resulting in a deeper and longer recession than we envisage for all other G7 economies

Samuel Tombs, chief economist at Pantheon Macroeconomics, is predicting the UK will officially enter a recession – as defined by two or more quarters in a row of falling output – by the end of the year.

GDP already shrank in the third quarter of 2022, with a 0.2% contraction, and Mr Tombs is predicting another 0.2% drop between October and December.

He said: “The Government looks set to pull back energy price support substantially next year, while higher interest rates will squeeze disposable incomes and spur households and businesses to pay off debt.

“As a result, we continue to expect a peak-to-trough fall in the quarterly measure of GDP of about 2%, and doubt that the economy will grow again until early 2024, resulting in a deeper and longer recession than we envisage for all other G7 economies.”

Trade data published separately by the ONS on Monday also showed that Britain’s trade deficit widened by £100 million to £23.9 billion in the three months to October 2022, with the value of goods exported in October down by 2.2% or £700 million and goods imported falling by 2.6% or £1.4 billion.

nline

nline